Though the chill began earlier, Investors have been decidedly frigid on banking stocks since the March crisis. A sharp selloff has left their valuations at 2020 levels – and that’s well below what their technicals and outlook merit, argues Eric Compton, Equity Strategist at Morningstar. For the April 2023 issue of Morningstar’s Financial Services Advisor, he authored a report entitled “Banking Outlook 2023: The Sector Is Cheap Again, Even if the Road Forward Won’t Be Easy.” The widespread negative sentiment toward banking stocks is creating excellent opportunities for investors willing to hold them for two to three years, says Compton. Institutional Investor asked him to explain why investors should see banking equities in a new light.

How severely are banking stocks currently undervalued?

Eric Compton: Banking stocks have had a 40% selloff since we last characterized them as fully valuated in our 2022 outlook, with much of that selloff occurring after the March 2023 banking crisis. But the drop in valuation for these equities isn’t nearly what the actual changes in fundamentals would justify.To put it in context, when I look at the banks I cover – especially the regionals – they’re trading at valuations that imply either permanent impairment of profitability, or significant equity raises, or some combination of the two. But what’s the probability of either of these things happening? Extremely low, in our analysis. And investors are being paid to take those risks. I believe banking stocks are going to have good absolute returns over the next couple of years.

The March banking crisis did a lot of damage…

Compton: Definitely. Banking stocks tend to be highly sentiment-driven because they’re so sensitive to economic developments. So investor psychology plays a huge role. The negative sentiment is mostly due to the March banking crisis, but to be fair, banks were selling off a bit even before March 8th amid debates about recession risks. Investors know banks typically do worse during recessionary periods, as they tend to be higher beta names that sell off in risk-off environments.

Where are the biggest misconceptions driving this investor pessimism?

Compton: Those that fuel anxieties that there will be a complete loss of confidence in the U.S. banking system, or that banks will see a permanent drop in profitability. Since the March crisis, every investor and analyst has been forced to become a bank analysis to a degree, and many aren’t highly knowledgeable about the accounting, regulatory requirements, how capital ratios works, and other fundamental aspects. They’re trying to catch up, and it’s creating a lot of confusion.Certainly, even the most informed investment firms are now far more focused on looking at unrealized losses on bank balance sheets, and then attempting to tie those into regulatory capital in different ways. So they start marking different parts of the balance sheet to market. But as you do that, capital gradually looks lower and lower, depending on how far you want to go.

On the more extreme side, where’s there more confusion, investors are worried about the health and resilience of the banking system at large. They see continued bank runs, deposit costs surging, and banks needing to replace deposits with debt, killing their profits. Their analysts are asking, “the March crisis may have started as an issue for a few select banks, but can it grow into a systemic issue where we’ll see runs on multiple banks – and cause people to lose confidence in the entire banking system? Has there been a sea change in the banking sector in which it will never be as profitable as it was before?”

According to our analysis and research, we doubt that these things will happen.

Can you give a few specifics on why?

Compton: Banks are more stable than investors realize. Several are coming off some of their highest earnings quarters ever, and you’re going to come down from that. It’s typical peak-of-the-cycle behavior.Regarding deposit runs, all the latest data suggests that deposit bases have stabilized after the initial drop on March 8th, and that’s important. Yes, we could still get a negative headline event that triggers more runs, but all the data says deposits are roughly stable.

How about rising deposits costs? Q1 results show some acceleration, but it was typical behavior you see at the end of any rate cycle. This tells me there’s some pressure on profitability, but nothing that the banking industry can’t deal with. In fact, none of the banks I cover are near the danger zone of being unprofitable.

As for regulatory worries, remember that regulators want a profitable banking sector. If I’m a regulator and I ask myself, “do I think that forcing banks to raise capital is going to improve confidence in the U.S. financial system?”, the answer is no. Further, none of the banks I cover are breaching any regulatory ratios, so it would be odd for regulators to just jump in and force them to raise capital in the hopes of improving confidence. The banks just haven’t done anything to warrant that.

So I don’t see the banking sector facing any kind of permanent impairment in profitability. Now, First Republic was an exception. When I ran the math on them, well before the crisis, I said “I don’t think these guys are going to be profitable,” I dropped my fair value down to $3 – when the market was still trading five or six times that and the median consensus on valuation was $55. So I’m not bullish on every bank.

What impactful regulatory changes do you see coming?

For one, I think regulators will change a rule to make banks include the AOCI, or Accumulated Other Comprehensive Income, when reporting unrealized losses from their available-for-sale securities. This will increase losses for banks. But I don’t see regulators doing this until middle or late 2024, and none of the banks under my coverage – even the ones that look the worst today – are going to breach any regulatory ratios even if you include AOCI.Overall, I think banks will have time to grow into the regulatory changes they’ll face. I don’t see any bad situations really playing out from that.

If commercial real estate tanks, how badly could that hurt the banking sector?

When I look at the exposures for the banks I cover which are most exposed to commercial real estate, a third of loans are to CRE. Of those, only roughly 10 to 20% are to office space. For many banks, we’re looking at 3% to 6% of loans going to office properties. And they’re underwritten at loan to values of 50% to 60%. This gives a lot of cushion before losses start to hurt your capital base.Of course, many banks will feel pain from losses in CRE – especially smaller banks that can have 40%or 50% of their loan book devoted to CRE, with 30% to 40% of those loans in office space. Those exposures would worry me. But the majority of the largest American bank have far less exposure to CRE, and I see their losses being manageable.

Which banks do you think are particularly good bargains?

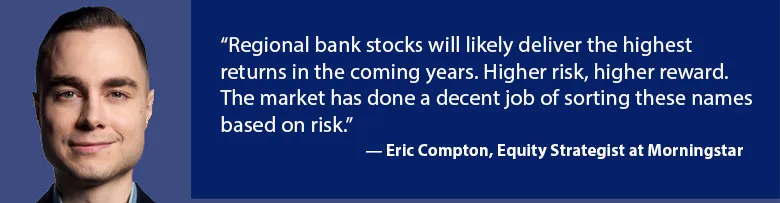

Compton: I like Citigroup. They’re one of the more challenged banks I cover, but also one of the cheapest, so you don’t need much to go right to see outperformance. And I like that they’re a globally systemically important bank, or G-SIB, so you won’t see the same deposit outflows or regulatory risks that some investors fear they’ll see in smaller regional banks.That said, regional bank stocks will likely deliver the highest returns in the coming years. Higher risk, higher reward. The market has done a decent job of sorting these names based on risk. if you’re looking for a safer pick that still has good upside, I’d look at M&T Bank. If you have greater risk tolerance, two banks I’d consider are Comerica and KeyBank. They probably only need to survive to deliver strong returns, and I think they will survive.

But I want to stress that these are long-term positions. Bank stocks are going to have a bumpy road in 2023. Over two or three years, though, I think many are going to outperform other sectors and hopefully the overall market.

Learn more about investment opportunities in banking equities.

Read more sector analysis on the II Communities on Equity Research & Market Insights