China’s economy may be slowing down, even though consumers haven’t stopped spending. Internal migration trends that are often hidden from government statistics may partly explain the conundrum.

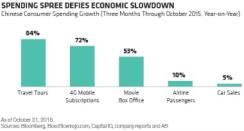

The Chinese consumer seems oblivious to the broader state of the economy. Whereas gross domestic product growth in China has fallen from 7.9 percent two years ago to 6.9 percent in the past quarter, retail sales growth has held firm at about 11 percent. Although sales growth of big-ticket items such as cars has been relatively modest, spending on smaller items and services such as movie tickets and mobile phone subscriptions has increased at a breakneck pace (see chart 1).

There are many explanations for the consumer’s resilience. China’s government is actively promoting policies to shift its economy toward consumption. Income per capita is rising, and the middle class is growing, driven by urbanization, which typically involves the movement of populations from rural areas to coastal cities.

But urbanization is a two-way street. In fact, we at AB believe that some of the strength in Chinese spending can be explained by people moving back to smaller cities after trying their luck in the large tier-1 cities, such as Shanghai and Beijing, where migrant workers often discover that life isn’t easy.

Beyond the bright lights of the big city, housing is very expensive, so workers often live in rundown neighborhoods with long commutes to work. Some welcome government incentives to look for opportunities back in third- and fourth-tier cities, where lower wages are offset by a lower cost of living, so disposable income remains the same or improves. These trends often fall below the radar of official government statistics that nourish the markets.

For example, take the story of Lin, a 24-year-old from Mianyang, a tier-3 city of 4.5 million, in Sichuan province. Lin’s parents moved to Shanghai seeking better education, health care and income. Their higher incomes were reflected as part of a trend that further widened the urban-rural disposable income gap (see chart 2).

When Lin followed his parents to Shanghai, however, he found that work was a struggle. He told us that he lived in a poor area, left home at 4 a.m. to commute to work and didn’t return until 9 in the evening. And he didn’t really fit in culturally with his new Shanghai acquaintances.

He returned to Mianyang after finding a job there with an online retail business. It paid 25 percent less than he had earned in Shanghai, but his rent was lower, and he had no commuting costs. So despite a decline in disposable income, Lin’s discretionary income actually increased. Lower-tier cities have developed dramatically in recent years, with modern transport infrastructure, Internet connectivity and excess apartment inventory that supports lower rents. Lin says he feels much more at home, and hasn’t really given up any of the comforts of big-city life.

Official data miss the nuance of Lin’s story — and of millions like him. Lin will be counted as having always lived in Mianyang, because his hukou, or household registration, hasn’t changed. It won’t reflect his move to Shanghai and back. Lin’s fall in income will appear as a slowdown in GDP growth, because his wages dropped when he left Shanghai. His rise in discretionary income — and better quality of life — won’t be visible at all to data analysts.

Of course, the economic slowdown in China is driven by many factors, primarily the sluggish industrial sector and weakening investments. To understand what’s really going on in China’s economy, though, you have to dig deeper. By looking beneath the surface, the dynamics of Chinese consumer spending can be revealed in ways that shed light on the government’s efforts to rebalance economic growth from the industrial sector toward the consumer.

Tassos Stassopoulos is portfolio manager of emerging consumer, global growth and thematic strategies at AllianceBernstein in London.

See AB’s disclaimer.

Get more on emerging markets.