For most of us, there is risk involved in pursuing a DIY method of doing nearly anything outside of our area of expertise. Nonprofit boards, like property owners hiring architects and contractors, can benefit from an outsourced chief investment officer’s (OCIO) technical expertise and resources in investment management, helping to ensure financial health and mission success. Here are some key considerations for nonprofits evaluating the value provided by outsourced chief investment officers (OCIOs) as their co-fiduciaries.

Is DIY really the most effective approach?

Being a steward of a nonprofit organization does come with fiduciary responsibilities. This is true even for volunteer board or investment committee members.

One could draw the analogy that nonprofit board and investment committee members and property owners are similar in that both wish to maintain the timelessness of their assets. A DIY execution of all the requisite work to build a home of one’s own is daunting and unnecessary—and could create a cycle of missteps and consequences that affect timetables, value, and confidence the job is being done right. For those reasons, property owners typically entrust experts to design, construct, and maintain their properties to achieve the desired outcome.

Many property owners often focus on how the property will be used and how they envision its design and leave the rest to others. Similarly, nonprofit board members’ primary focus can be to direct the investment objectives and long-term spending policy, but they don’t need all the skills to manage a nonprofit investment portfolio if they outsource the necessary expertise to an OCIO. Due to the size of most OCIO firms, they can serve as nonprofit organizations’ architect, general contractor, and property manager in the following ways:

The analogy presented may be particularly important to volunteer board and investment committee members who advance a nonprofit’s mission by selflessly sharing their experience, strategic advice, time, and financial support. However, when tasked with fiduciary responsibilities as stewards of a nonprofit investment portfolio, it is our view that outsourcing investment management responsibilities merits thoughtful consideration. Portfolio design, ongoing investment research and risk oversight responsibilities are not part-time endeavors. Instead, the board and investment committee should structure governance roles with direct oversight of the OCIO’s ongoing activity. By meeting with the OCIO to review performance, positioning, and risk on periodic basis (typically quarterly or semi-annually) the board can fulfill its fiduciary duty and improve the depth of its research and risk monitoring capabilities.

Are OCIOs worth the cost?

In our view, smaller endowments and foundations are increasingly acknowledging the limited bandwidth of volunteer investment committees and see value in fee-efficient OCIO models. For example, according to Cerulli Associates’ 2024 OCIO Providers Survey, among the largest 30 OCIO respondents, OCIO advisory fees are typically between 0.21% and 0.30% per year for nonprofits with $51 million to $100 million of assets under management (AUM). Assuming $100 million of AUM in a nonprofit portfolio, this translates to an OCIO cost of $210,000–$300,000 per year, which is significantly less expensive than staffing a full-time investment team to fulfill fiduciary responsibilities of ongoing research and risk oversight. Hiring an OCIO firm is potentially a highly effective way to access significant resources at a reasonable cost.

Is there benefit to having an OCIO with nonprofit experience?

Yes. Not only can OCIOs help you compare how your organization may be similar or different from your peers, but they also may provide non-investment related benefits such as custody services, philanthropic-focused consulting services, and reporting services.

What is the difference between advisory/consultant models and OCIO providers?

Some nonprofits choose to use an investment consultant to advise their investment committee on strategic issues and implementation. Often consultants provide “blueprints” (strategic advice) and recommendations for “sub-contractors” (a selection of fund managers to implement the strategic advice), but the investment committee is left to piece it all together. In other words, in these relationships, the investment committee retains responsibility to be the general contractor and property manager. This can be a useful for investment committees with more embedded investment experience and more time to work through the investment operations and risk oversight.

OCIOs, in contrast, build and manage the whole portfolio on a day-to-day basis on behalf of the investment committee. This can provide valuable time back to the investment committee to focus on more strategic issues such as fundraising and grant strategy. Allowing OCIOs day-to-day investment discretion (within agreed upon guidelines) also facilitates more nimble decision-making. This is a critical differentiator relative to the consultant model. We often see that investment committees that meet monthly or quarterly struggle to make timely investment decisions and struggle to quickly respond to ever-evolving market dynamics. OCIOs, however, are continuously monitoring market risks and opportunities and can quickly adapt portfolio positioning during volatile markets.

From DIY to strategic partnership

For volunteer nonprofit boards and investment committees, it may be beneficial to consider alternatives to a DIY approach to investment management—especially considering a nonprofit board’s fiduciary responsibilities.

Boards and investment committees should evaluate their skills, resources, and available time to focus on research, implementation, and risk oversight. If they find they cannot dedicate sufficient time to managing and overseeing assets on a day-to-day basis, OCIOs can be an excellent partner. Not only do OCIOs serve as co-fiduciaries, providing an additional layer of accountability that investments are managed in the best interest of the organization, but they also act as an extension of staff. This partnership allows the board and investment committee more time to focus on other critical issues that support the nonprofit’s mission.

So, the next time you feel compelled to do a portfolio “renovation” or check on the “plumbing and wiring” of our nonprofit’s investment portfolio, envision what our DIY outcome may look like. Would the outcome satisfy your Board’s fiduciary responsibility? If not, an OCIO partnership may be a lighter and more cost-efficient lift to take you to the next level.

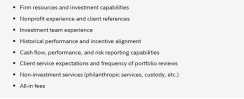

Questions volunteer investment committees should ask of their OCIO

To fulfill their fiduciary responsibilities, investment committees should conduct thorough due diligence when engaging with any consultant or OCIO provider. If an investment committee decides to delegate day-to-day management and oversight to an OCIO, we have compiled a non-exhaustive list1 of topics investment committees should consider before selecting an OCIO partner:

As a best practice, we recommend investment committees explore these topics by conducting a request for proposal (RFP)2 and interview process every three to five years to ensure their OCIO provider or consultant remains competitive relative to peers.

Learn more about Fidelity’s Outsourced CIO Solutions

Erika Murphy is a portfolio manager in the Global Institutional Solutions (GIS) group at Fidelity Investments. In her role, she designs and manages custom multi-asset class mandates for institutional investors including endowments, foundations, and nonprofit organizations. The team is dedicated to serving the needs of institutional asset owners that seek support in strategic asset allocation, ongoing portfolio management, and customized portfolio design and implementation.

Danielle Frissell is a senior vice president of the endowments & foundations business in the Institutional Client Group at Fidelity Institutional®. Fidelity Institutional is a division of Fidelity Investments that offers investment insights, strategies, and solutions to institutional investors. In this role, Ms. Frissell is responsible for new business development and relationship management activities with endowments, foundations, and non-profit institutions.

To access more content please visit Fidelity’s Communities on Alternative Investments.

1This list is not meant to be exhaustive, but rather a suggestion of starting points for investment committee due diligence.

2The Request for Proposal (RFP) process is a formal method used by organizations to solicit proposals from potential vendors or service providers.

Unless otherwise expressly disclosed to you in writing, the information provided in this material is for educational purposes only. Any viewpoints expressed by Fidelity are not intended to be used as a primary basis for your investment decisions and are based on facts and circumstances at the point in time they are made and are not particular to you. Accordingly, nothing in this material constitutes impartial investment advice or advice in a fiduciary capacity, as defined or under the Employee Retirement Income Security Act of 1974 or the Internal Revenue Code of 1986, both as amended. Fidelity and its representatives may have a conflict of interest in the products or services mentioned in this material because they have a financial interest in the products or services and may receive compensation, directly or indirectly, in connection with the management, distribution, and/or servicing of these products or services, including Fidelity funds, certain third-party funds and products, and certain investment services. Before making any investment decisions, you should take into account all of the particular facts and circumstances of your or your client’s individual situation and reach out to an investment professional, if applicable.

Investing involves risk, including risk of loss.

Diversification and asset allocation do not ensure a profit or guarantee against loss.

Registered investment products (including mutual funds and ETFs) and collective investment trusts managed by Fidelity Management Trust Company (FMTC) are offered by Fidelity Distributors Company LLC (FDC LLC), a registered broker-dealer.

Fidelity Institutional Asset Management (FIAM) investment management services and products are managed by the Fidelity Investments companies of FIAM LLC, a U.S. registered investment adviser, or Fidelity Institutional Asset Management Trust Company, a New Hampshire trust company. FIAM products and services may be presented by FDC LLC, a non-exclusive financial intermediary affiliated with FIAM and compensated for such services.

Fidelity Investments is an independent company, unaffiliated with Institutional Investor LLC. There is no form of legal partnership, agency affiliation, or similar relationship between your financial advisor and Fidelity Investments, nor is such a relationship created or implied by the information herein.Fidelity Investments is a registered service mark of FMR LLC. Fidelity Investments® provides investment products through Fidelity Distributors Company LLC; clearing, custody, or other brokerage services through National Financial Services LLC or Fidelity Brokerage Services LLC, Members NYSE, SIPC; and institutional advisory services through Fidelity Institutional Wealth Adviser LLC.

1189722.2.0