Bubbles of money and growth graph with cityscape background, Bubble of economy concept

Credit: pixbox77/Getty Images/iStockphoto

Today it’s possible to use artificial intelligence to create the full range of mission-critical organizational functions necessary to run an asset allocator, asset manager, or investment consultant. Whether or not the industry is ready for such a disruptive use of technology is a separate question, but I believe the idea is worth exploring.

This application of AI — what I like to call investment management in a box — uses large language models as its core reasoning and decision-making engine to simulate humanlike behavior and thinking within a virtual environment. These LLM-driven agents are a notable improvement over traditional rule-based or AI chatbots, offering greater flexibility, realism, and cognitive complexity in modeling human activities and interactions.

A handful of institutional investors are developing LLM single-agent systems, including BlackRock’s unfortunately named Thematic Robot and Morgan Stanley’s AskResearchGPT.

Certainly, this goes a step beyond chatbots, but a genuinely visionary view recognizes that the transformative power of LLMs is realized when LLM-powered single agents are combined into multiagent systems.

Unlike single-agent systems, a multiagent system, or MAS, is a network of domain-specific AI agents, each with unique skills and knowledge. These agents, much like humans, collaborate, communicate, negotiate, and adapt in real time to changes in the environment. They perform tasks, solve problems, and achieve complex goals that would be challenging for a single agent to accomplish. Critically, agents continually collect data from their environment, enabling them to adjust their actions and strategies as needed to ensure the system remains responsive and resilient. This adaptability is particularly valuable in scenarios requiring real-time decision making.

To initialize agents individually, developers use prompts that contain detailed descriptions of their behavior, function, preferences, memories, and relationships.

Here’s a naive example of how a multiagent system, which comprises a product agent, a marketing agent, and a legal agent, works in concert to write a press release about a new investment product: The product agent provides updates on the investment and sends them to the marketing agent, which drafts a press release. The draft is then sent to the legal agent for review, which, if necessary, collaborates directly with a human lawyer to approve the final version.

Developers can endow individual agents with personality profiles that affect their linguistic styles, strategic behaviors, and overall consistency. As with humans, the personalities significantly influence how multiagent LLMs interact. The ability to shape these profiles allows for more nuanced and realistic simulations of human interactions between agents.

Multiagent systems can take different forms depending on their objectives:

- Cooperative systems: Agents have common goals and cooperate to achieve them.

- Adversarial systems: Agents have opposing objectives and compete to achieve them.

- Mixed-agent systems: Agents combine elements of both cooperation and competition.

- Hierarchical systems: Higher-level agents oversee and coordinate the actions of lower-level agents to achieve a common goal.

- Heterogeneous systems: Agents with different expertise or functions work together to achieve complex objectives.

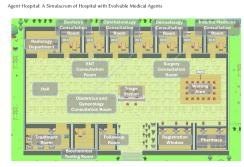

“Agent Hospital simulates the whole closed cycle of treating a patient’s illness: disease onset, triage, registration, consultation, medical examination, diagnosis, medicine dispensary, convalescence, and post-hospital follow-up visit.” Figure 1 gives an overview of Agent Hospital.

Figure 1.

Source: Agent Hospital: A Simulacrum of Hospital With Evolvable Medical Agents.

Each patient agent has distinct demographic information and may get a disease randomly. The 14 doctor agents are engineered to diagnose diseases and create detailed treatment plans, whereas the four nursing agents focus on triage, supporting day-to-day therapeutic interventions. Figure 2 gives examples of the demographic information.

Figure 2. Demographic Information

Source: Agent Hospital: A Simulacrum of Hospital With Evolvable Medical Agents.

The authors propose a strategy in which doctors learn from a medical records library and their agents’ experiences. Successful cases are used for future interventions and stored in the medical records library.

The strategy allows the doctor agents to “evolve,” meaning they “can keep improving treatment performance over time without manually labeled data, both in simulation and real-world evaluations,” leading to superhuman accuracy in treatment orders.

“After treating about ten thousand patients — it could take real-world doctors more than two years to do this — the evolved doctor agent achieved an accuracy rate of 93.06 percent” on major respiratory diseases. Human experts in the data set had an accuracy rate of about 87 percent. (The data, MedQA, is a medical text question-and-answer data set containing multiple-choice questions drawn from medical licensing exams in the U.S., mainland China, and Taiwan.)

Although they acknowledge the need for future research, the authors of the paper found that “Agent Hospital demonstrates promising scalability and interactivity, making it suitable for more complex medical simulation experiments.”

The Agent Hospital paper and other studies demonstrate that if correctly designed, LLM-based multiagent systems can convincingly and realistically simulate human behavior, which leads me to believe that a similar system could be used to create a simulation of an investment management enterprise in which all the actors are autonomous LLM-powered agents.

Let’s call it Agent Investor and make it a U.S.-based Securities and Exchange Commission–registered investment management company offering a long-only U.S. large-cap equity strategy that seeks to provide risk-adjusted returns exceeding the S&P 500 Total Return Index. (We could modify this for an asset allocator or investment consultant.)

We begin by creating specialized agents to handle the critical organizational roles of the company’s operations:

- Investment agent: Designs, trains, and optimizes an investment model that seeks to provide the desired investment returns.

- Portfolio management agent: Implements the investment model’s output, manages positions, and ensures proper asset allocation.

- Market analysis agent: Continuously analyzes the U.S. equity market, providing real-time insights to the real-life model and portfolio manager.

- Risk management agent: Monitors and manages portfolio risk to ensure risk-adjusted returns meet objectives.

- Compliance agent: Ensures the firm adheres to regulatory requirements.

- Sales agent: Markets the company and its products to potential and current investors.

- Investor relations agent: Manages relationships with clients and investors, ensuring clear communication and reporting.

- Human resources agent: Manages recruitment, training, employee well-being, and organizational development to ensure that the company attracts and retains top talent.

- Information technology agent: Applies technology to solve and optimize organizational issues at scale.

- Chief executive officer agent: Oversees all aspects of the company’s operations.

- Chief investment officer agent: Oversees the firm’s entire investment process and strategy.

- General counsel agent: Provides legal advice and guidance to the company’s executives and management team and oversees all legal matters that arise within the organization.

- Investment committee agent: Oversees and manages investments on behalf of the organization.

- Operations agent: Oversees the day-to-day operations of the firm, ensuring that trading, IT systems, and internal processes run smoothly and efficiently.

- Chief financial officer agent: Manages the company’s financial actions.

- Marketing agent: Develops and executes the company’s marketing and client acquisition strategy, building the brand to attract institutional and high-net-worth clients.

The result is an investment management business in a box.

There would also be sub-agents to help fulfill their principals’ duties; the CFO, for example, could have sub-agents responsible for such tasks as accounting, budgeting, payroll and taxes, and treasury management.

Like the doctors in Agent Hospital, the agents would communicate, collaborate, adapt to changes in their environment, and learn from their experiences.

Some readers might argue that our Agent Investor is a chimera because ultimate fiduciary authority must rest with human actors. So let’s create Agent Investor with a hierarchical agentic structure in which all agents report to a C-suite of humans, who oversee the agents’ activities and make the final critical decisions.

Others may claim our simulacrum is unrealistic because an MAS cannot autonomously create and implement an investment strategy. Although there is increasing evidence that agents can perform such tasks, for the sake of argument, let’s remove the Investment Agent from our simulation and assume that the investment organization uses a human-based investment strategy.

Such multiagent systems can be created with existing AI. One example of the state of readiness is Altera’s Project Sid, in which thousands of autonomous AI agents, each with specialized professions and personalities, collaborate to create virtual AI civilizations with their own governmental institutions, economies, cultures, and religions. Robert Yang, a former MIT professor and the founder of Altera, acknowledges that although Project Sid is starting with game simulations, the results demonstrate that “we’re solving the deepest issues facing agents: coherence, multiagent collaboration, and long-term progression.”

For all their promise, these systems come with significant technical challenges, including specifying appropriate learning goals, scalability and performance, costs, hallucinations, operational complexity, explainability and transparency, and data privacy and security.

Yet other industries are successfully dealing with these challenges and creating and implementing multiagent systems to enhance manufacturing processes, manage supply chains, and improve IT systems. Some financial services firms also use specialized MAS for fraud detection and financial monitoring.

The investment industry is eager to deploy LLMs as trading bots and co-pilots, but even the idea of allowing AI systems to independently make critical investment and business decisions is currently a bridge too far.

The primary obstacle to adopting MAS and advanced AI is not technical or operational but rather the behavioral bias that says investing is inherently a human activity. As Michael Taylor of Coldwater Economics puts it: “My starting point is that, one way or another, investing is and will remain a fundamentally human activity.”

Until we can overcome this algorithm aversion, LLMs will remain AI-powered assistants that provide analysis and context, with humans making the final decisions.

And we all know how well this has worked.

Angelo Calvello, Ph.D., is co-founder of Rosetta Analytics, an investment manager that uses deep reinforcement learning to build and manage investment strategies for institutional investors.