Private alternatives offer returns and diversification benefits amid volatility and risk

Study of 250 allocators in EMEA representing $10tn AUM unearths private alternatives allocation plans: Download the research here.

Private market allocations are set to increase among institutional investors in Europe and the Middle East in the backdrop of growing geopolitical risks and spikes in market volatility, according to new research from PGIM and Institutional Investor’s Custom Research Lab.

Data from the PGIM/II study, What’s Your Alternative? found that private alternatives comprise approximately 25% of the portfolios of the 250 institutions surveyed in the study managing $10 trillion in assets under management.

Within this allocation, real estate equity (18%), private credit (11%), private equity (10%), and real estate debt (10%) are the alternative asset classes held most widely. Investors in the study anticipate increasing their holdings in these and other private asset classes in the years ahead.

“Our private asset allocation is driven by the diversification benefits of the asset class as we are heavily exposed to equity market volatility in our portfolio. Moreover, there has been a greater focus on investing in income-producing alternative assets in the last few years,” says a pension director at a $10 billion pension in the United Kingdom.

The study's investment decision-makers anticipate increasing their risk appetite, which suggests a healthy outlook for further investment in private market assets.

More than 75% of survey respondents plan to increase their allocations to private alternatives over the next two years. Investors say they’re especially likely to increase their allocations to private credit (44%) and real estate debt (42%) to capture the coupon payments from the current high interest rates and illiquidity premium such assets typically offer.

Investors’ rationale for private market investments stems from the strong historical performance of private alternative assets and their insulation from the vagaries of publicly traded assets such as equities and fixed-income assets.

Fully 88% of study participants say they look to private alternatives to generate income through interest payments or dividends, and 82% seek returns through asset appreciation.

Private alternative assets also deliver diversification and risk control benefits to institutions in Europe and the Middle East as 88% of respondents say they’re very or somewhat likely to use private alts to manage risks, and 71% say they use them for capital preservation to hedge against downside risks.

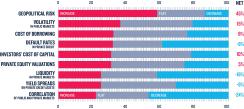

A solid majority of investors in the PGIM/II study say they anticipate an increase in geopolitical risk and public market volatility in the next two years. The study was conducted during the summer of 2024 – before the US election – and it seems likely that the incoming administration’s eagerness to recast U.S. tariff and trade policy will bring new risks and volatility to public markets.

Geopolitical risk and market volatility will increase

What is your two-year outlook for the following investment factors?

Against this backdrop, investments in private assets may be a sound strategy, especially for long-term institutional investors, as such assets are priced infrequently and insulated from volatility inherent in daily revaluation under mark-to-market rules.

Increased Allocations

Investors are likely to increase their private credit allocations in an effort to take advantage of shifts in the commercial banking environment, as regulators have raised requirements for capital reserves and loan documentation. As a result, bank loans for business expansion are less available and take longer to arrange. Unlike bank lending, private credit solutions are tailored to meet borrowers’ particular needs, rather than the documentation-heavy, one-size-fits-all model from commercial banks. Today, private credit managers serve more segments of corporate lending, a wider range of real asset debt, and a broader set of asset-backed loans including those backed by intangible assets such as music royalties and litigation finance.

The environment of high interest rates in the wake of the global inflationary shock has also separated private credit issuers with strong business models that have robust balance sheets and can support higher interest expenses from their less prosperous peers. As a result, senior secured lending currently offers the potential to capture unprecedented double-digit yields.

The PGIM/II study argues that the “real estate sector is transitioning from a distressed situation scenario to a growth-supporting environment,” which bodes well for new investment in property among institutional investors. It cites demand for new data centers in Europe and Middle East along with need for retirement facilities for the aged and affordable housing in cities as principal drivers of demand for capital in these regions. Meanwhile, regulators are calling for higher capital reserves among the region’s commercial banks, which places private lenders in a strong position amid the expected shortage of conventional bank loans in these sectors. Echoing their risk-on posture, study participants show the greatest interest in increasing their allocations to core plus and value-add strategies in real estate investments over the next two years. They are notably less interested, however, in high-risk opportunistic real estate investments.

Find out more: Access the full research report.

This is the first of three articles on the use of private market alternative assets among investors in Europe and the Middle East. In the weeks ahead, look for further discussion of private alternatives, investors’ risk and geographic concerns, and their preferences when selecting asset management partners for private market allocations.