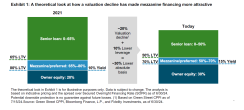

An estimated 20% decline in property values in recent years has allowed many nontraditional lenders to offer financing in the mezzanine market using less leverage and at a 30% lower absolute basis [see Exhibit 1]. Mezzanine debt, a significant and growing segment of private credit, offers the potential for elevated yields and historically attractive risk-adjusted returns. However, synthetic mezzanine structures carry margin call risk, whereas direct mezzanine debt does not.

Joining Fung for the discussion was Andy Rubin, Institutional Portfolio Manager, Fidelity Investments, where he assists portfolio managers and their CIOs in ensuring portfolios are managed in accordance with client expectations.

What’s the backdrop in commercial real estate that might make mezzanine debt appealing to investors?

Andy Rubin: If you exclude office space, commercial real estate has looked healthy overall, backed by low vacancy rates, steady rents, and strong cash flows. That said, lower property values in several segments, interest-rate uncertainty, and the desire for banks to lower their leverage ratios have made many traditional lenders selective about the loans they offer.

While some have exited the sector, many of the more than 4,000 banks in the U.S. remain active along with insurance companies at lower leverage levels. This has created an expanded opportunity set for mezzanine debt providers to replace a piece of the capital structure – and for investors to potentially generate equity-like returns at modest risk.

Current real estate values are down more than 20% from recent peaks, and it is possible they could decline further. Direct mezzanine debt is positioned to take advantage of current market conditions. This investment strategy has offered equity-like returns, while maintaining 30% equity cushion based on 2024 reset values. Our direct mezzanine structure also avoids financial leverage at a time of uncertainty.

You mentioned your direct mezzanine structure. Can you explain how the direct and synthetic approaches differ?

Fung Lin: The direct approach provides an unlevered mezzanine loan in partnership with banks, insurance companies and other balance sheet lenders, who provide the first of two separate loans. With the direct approach, the mezzanine loan can be floating rate or fixed rate. This can be advantageous to lock in current high base rates.

The synthetic approach originates a whole loan and finances the loan with another lender, while retaining the “synthetic” mezzanine risk tranche of the loan. This is sometimes referred to as the levered whole loan model. The loan is typically floating rate, and this model is similar to a regional bank business model, where effective management of liabilities – say deposits for banks and a secured line of credit for debt funds – becomes more important, especially in market downturns.

So why does Fidelity favor the unlevered mezzanine structure?

Lin: Under both structures, the underlying credit risk is the same. On the risk management side, unlevered mezzanine loans mean there is no margin call risks during times of market volatility such as the covid pandemic, or large secular change like the decline in office demand. On the return side, rather than being forced to choose among a few select lenders, we can partner with the most cost-effective among thousands of senior balance-sheet lenders in the market. The combined economics of such a partnership allows direct mezzanine lenders to keep as extra yield some of the excess economics that otherwise would go to other participants in the capital structure.

In addition, a borrower may have strong bank relationships or existing low-cost fixed rate debt in place. We have the flexibility to be a partner in those situations, too.

Rubin: Fidelity has been focused on the direct mezzanine investment model for more than 17 years, so we have a strong reputation and origination network within the market. Our ability to engage the entire senior mortgage market and have structural control of our mezzanine loans often provides the most flexible, cost-efficient option to a borrower. In the current de-levering environment, there is also significant opportunity to help borrowers pay down existing loans to modest levels with direct mezzanine loans.

To sum it up, what should investors take away from this conversation?

Rubin: Broader real estate market de-leveraging is happening as low-rate loans mature into a higher-interest rate environment coupled with banks retrenching. There is over $2 trillion of real estate debt that is maturing in the next three years, providing many opportunities to be selective as an investor. While it’s difficult to call a bottom in real estate values, a direct mezzanine debt approach is not reliant on property price appreciation. We believe the current market provides an attractive entry point irrespective of the go-forward trajectory of property values. More specifically, we believe an unlevered mezzanine debt approach can offer equity-like returns with modest credit risk.

Learn more about Fidelity’s growing lineup of alternative investments.

Information provided in, and presentation of, this document are for informational and educational purposes only and are not a recommendation to take any particular action, or any action at all, nor an offer or solicitation to buy or sell any securities or services presented. It is not investment advice. Fidelity does not provide legal or tax advice.

Before making any investment decisions, you should consult with your own professional advisers and take into account all of the particular facts and circumstances of your individual situation. Fidelity and its representatives may have a conflict of interest in the products or services mentioned in these materials because they have a financial interest in them, and receive compensation, directly or indirectly, in connection with the management, distribution, and/or servicing of these products or services, including Fidelity funds, certain third-party funds and products, and certain investment services.

This content contains statements that are "forward-looking statements," which are based upon certain assumptions of future events. Actual events are difficult to predict and may differ from those assumed. There can be no assurance that forward-looking statements will materialize, or that actual results will not be materially different from those presented.

Information presented herein is for discussion and illustrative purposes only and is not a recommendation or an offer or a solicitation to buy or sell any securities. Views expressed are as of the date indicated, based on the information available at that time, and may change based on market and other conditions. Unless otherwise noted, the opinions provided are those of the authors and not necessarily those of Fidelity Investments or its affiliates. Fidelity does not assume any duty to update any of the information.

Past performance is no guarantee of future results. Investing involves risk, including risk of loss.

Fidelity Investments provides investment products through Fidelity Distributors Company LLC and clearing, custody, or other brokerage services through National Financial Services LLC or Fidelity Brokerage Services LLC (Members NYSE, SIPC).

© 2024 FMR LLC. All rights reserved

1165642.1.0