AUTHORS

Aaron Sack, Head of Morgan Stanley Capital Partners

Patrick Whitehead, Executive Director, Morgan Stanley Capital Partners

KEY TAKEAWAYS

- Mid-sized private equity investments have generated outsized relative revenue and EBITDA growth.

- Sponsors need a unique strategy and approach to succeed in the dynamic middle-market landscape.

- Focusing on founder-owned or founder-involved companies can be a source of repeatable alpha.

- Founder deals often have a unique and diversified set of value creation opportunities.

- Succeeding with founder investments requires the right culture, approach and incentives.

In the past two decades, private equity (PE) has grown from a relatively niche asset class to one that has become increasingly competitive, with a plethora of new offerings. Dedicated strategies are now offered for large-cap, mid-sized, and small-cap companies—and everything in between, with more PE managers emerging every year.

In this increasingly crowded asset class, we believe that the middle market can be a differentiated source of alpha—especially for companies with founder involvement. But we believe that generating alpha in the middle market requires a manager with specialized capabilities, a rigorous due diligence approach, and a proven playbook for creating value in the sector. Such expertise becomes even more crucial when partnering with entrepreneurs and business founders. In this paper, we outline why we see significant potential in this approach to the middle market, and begin with a review of the middle market’s competitive track record thus far.

1 IMPORTANT: This material is a general communication, which is not intended to be impartial, and reflects the beliefs of Morgan Stanley about certain market factors for which others may have different views. All information provided has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy. See other important disclaimers at the end of this material.

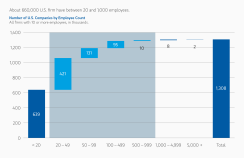

While PE as an asset class has consistently generated strong asset-level returns, the middle market has emerged as a particularly attractive place to invest, given the immense supply of privately owned targets and the greater potential for outsized value creation. At the end of 2022, there were approximately 660,000 firms in the U.S. with 20-1,000 employees, representing a fertile hunting ground for sponsors focused on the middle market (Figure 1).

(census.gov))

At the same time, Morgan Stanley’s proprietary data on market-level PE returns indicates that sponsors may drive significantly greater relative revenue and EBITDA growth in U.S. middle-market investments, compared with large-cap deals (Figure 2).

What explains the competitive track record of PE investments in small to mid-sized companies? We have identified several structural features that we believe enhance the potential for sustained alpha generation.

- First, by definition, middle-market investments usually have a small market share, creating significant headroom for organic growth through new customers, new products, new markets, or a combination of all three. In contrast, mature market leaders typically have limited potential for future growth.

- Second, middle-market companies often have significant opportunities to expand margins by scaling up to reduce vendor costs and driving corporate efficiency as the business grows.

- Finally, middle-market companies often operate in fragmented industries, and are of a sufficiently small scale that add-on acquisitions can drive meaningful equity value creation. In contrast, M&A in more consolidated, mature markets often does not move the needle as meaningfully.

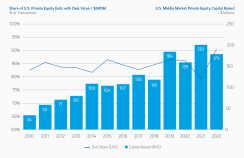

In our view, these advantages have attracted growing interest among investors. Since 2010, the annual capital raised for middle-market investing has increased from $34 billion to $179 billion, and the share of total PE exits made up by middle-market transactions has increased from 82% to 90% (Figure 3).

Source: Pitchbook Q2 2023 Annual U.S. Private Equity Report

With so much attention and capital flowing into the middle market, the average PE auction process has become more competitive, and the margin of error has compressed.

The appeal of founder-involved deals

As a result, we believe that sponsors are under increasing pressure to identify and specialize in sub-segments of the market where the equity value creation opportunity is greatest. Sponsors will need an additional edge that can help drive top-quartile performance. We believe that edge can be found by partnering directly with company founders, whose companies can be a source of sustainable alpha in the middle market. This is illustrated in Figure 4, which shows how over a broad market sample of 129 U.S. middle-market PE exits between 2007 and 2023, founder-involved

investments drove significantly greater relative revenue and EBITDA growth compared to non-founder investments.

We see a number of benefits to founder-involved investments that are more pronounced than in a standard middle-market PE investment.

Partnering with founders often goes hand-in-hand with providing the first institutional capital to a family-owned business. Thus, important groundwork begins pre-investment—founder recapitalizations often entail bilateral negotiations or limited sale processes. This means competition for each asset can be lower, and sponsors often have more time to assess the business and develop strong relationships with management.

After closing, founder-involved transactions present greater opportunities to execute quick wins and professionalize the business, in our view. Unlike companies that have been owned by institutional investors for multiple chapters, founder-owned businesses often have a greater opportunity to grow revenue, expand margins, and build teams in the early days of an investment.

Finally, we believe that founders usually feel a very strong sense of loyalty to their companies and are typically highly motivated to solidify their legacy and reputation. Founder enthusiasm and support are assets that can help drive growth in many ways, both tangible and intangible. These include building strong customer relationships, identifying and nurturing add-on acquisition targets, and serving as an ambassador for future investors.

A specialized approach and toolkit

To fully unlock the alpha embedded in many founder-owned businesses, we believe that sponsors need a specialized skill set relative to a standard PE transaction and a collaborative working style—one that can maximize results and mitigate risks.

To start, we believe that sponsors must be prepared to deliver comprehensive support. Because many founder-involved transactions are not marketed broadly by sophisticated intermediaries, sponsors may need to manage the full end-to-end diligence process internally and work with a flexible timeline that many founders require.

In the early days of a new founder-involved investment, sponsors may need to dedicate real time and effort to developing genuine relationships with management. Such relationships, in our view, are crucial to help drive the significant change that frequently comes with a PE investment, given the outsized influence founders often have on the operations and culture of their business. To facilitate this cooperation, we believe that incentives need to be aligned to keep the founder fully engaged. A good incentive model balances the founders’ requirements for near-term liquidity while maintaining sufficient financial “skin in the game” for them to stay engaged for the next chapter of the investment.

As the investment moves into the value creation planning and execution stage, it is critical for the sponsor to appraise— and complement—the founder’s management strengths. For example, the archetypal founder-owned business has a strong product, value proposition and customer relationships.

But often, the founder has not sought out external perspectives and best practices from their industry or others. At this crucial stage, we believe that effective sponsors will have an established toolkit to provide tangible support. Whether through strategies and tactics that can drive organic growth, price optimization, cost reduction, system/process centralization or team building, we believe that this is where the sponsor/founder partnership can take the business to the next level—both in financial performance and ultimately equity value creation.

The role of founder-owned PE investments going forward

We believe middle-market PE will continue to be a dynamic investment landscape as sponsor competition and new fundraising remain robust, transaction volumes continue to normalize after the 2022-2023 disruption, and the macroeconomic environment continues to have pockets of uncertainty and volatility. In our view, to generate sustainable alpha, PE sponsors need a differentiated strategy and hands-on operational toolkit.

We believe that founder-owned and involved businesses create an opportunity for sponsors to drive

sustainable outperformance. The supply of founder-owned companies that will be potential PE acquisition targets is expected to keep growing, as the U.S. Baby Boom generation continues to move into retirement age. By 2030, 73 million Americans are projected to be 65 years of age or older, and many of these founders and family owners will be looking for a business transition and a personal liquidity event (Figure 5).

We believe that founder-owned assets create differentiated opportunities for value creation and serve as an effective complement to standard middle-market transactions within a PE portfolio. In our view, they offer distinct benefits that come from partnering and aligning with owners to drive the next chapter of their business. We believe that succeeding with founder-owned companies requires a specialized strategy and approach that focus on building genuine relationships, aligning incentives, and deploying a tested operational toolkit to drive on-the-ground business building and value creation.

IMPORTANT INFORMATION

The views and opinions and/or analysis expressed are those of the authors as of the date of preparation of this material and are subject to change at any time without notice due to market or economic conditions and may not necessarily come to pass. Furthermore, the views will not be updated or otherwise revised to reflect information that subsequently becomes available or circumstances existing, or changes occurring, after the date of publication. The views expressed do not reflect the opinions of all investment personnel at Morgan Stanley Investment Management (MSIM) and its subsidiaries and affiliates (collectively “the Firm”), and may not be reflected in all the strategies and products that the Firm offers.

Forecasts and/or estimates provided herein are subject to change and may not actually come to pass. Information regarding expected market returns and market outlooks is based on the research, analysis and opinions of the authors. These conclusions are speculative in nature, may not come to pass and are not intended to predict the future performance of any specific strategy or product the Firm offers. Future results may differ significantly depending on factors such as changes in securities or financial markets or general economic conditions.

This material has been prepared on the basis of publicly available information, internally developed data and other third-party sources believed to be reliable. However, no assurances are provided regarding the reliability of such information and the Firm has not sought to independently verify information taken from public and third-party sources.

Alternative investments are speculative and include a high degree of risk. Investors could lose all or a substantial amount of their investment. Alternative investments are suitable only for long-term investors willing to forego liquidity and put capital at risk for an indefinite period of time. Alternative investments are typically highly illiquid – there is no secondary market for private funds, and there may be restrictions on redemptions or assigning or otherwise transferring investments into private funds. Alternative investment funds often engage in leverage and other speculative practices that may increase volatility and risk of loss. Alternative investments typically have higher fees and expenses than other investment vehicles, and such fees and expenses will lower returns achieved by investors.

This material is a general communication, which is not impartial and all information provided has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy. The information herein has not been based on a consideration of any individual investor circumstances and is not investment advice, nor should it be construed in any way as tax, accounting, legal or regulatory advice.

Charts and graphs provided herein are for illustrative purposes only. Past performance is no guarantee of future results.

The whole or any part of this material may not be directly or indirectly reproduced, copied, modified, used to create a derivative work, performed, displayed, published, posted, licensed, framed, distributed or transmitted or any of its contents disclosed to third parties without the Firm’s express written consent. This material may not be linked to unless such hyperlink is for personal and non-commercial use. All information contained herein is proprietary and is protected under copyright and other applicable law.

3874001