Mitesh Sheth, Multi-Asset Chief Investment Officer, Newton Investment Management

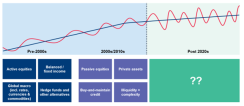

We have come to define the period that followed the 2008 global financial crisis and continued until the Covid pandemic in 2020 as the era of quantitative easing (QE) – a period in which financial markets were buoyed by ultra-low nominal interest rates and central-bank asset purchases. Investors benefited from net long positions in almost any risk asset as QE lifted all boats. That tide has now receded and threatens to expose weaknesses in portfolios.

During the QE period, many asset owners chose to switch into passive equities, as well as opting for buy-and-maintain credit strategies. Furthermore, many increased their allocation to more illiquid assets such as infrastructure, real estate and private equity, seeking diversification benefits and the potential for higher returns than those delivered by traditional markets.

Liquidity Supported Equities in Last Decade

S&P 500® total return vs. change in Federal Reserve (Fed) balance sheet, indexed to 1

As QE came to an end, the combination of unprecedented fiscal and monetary stimulus in response to the pandemic led to high and persistent inflation, and central banks then aggressively raised interest rates as they sought to contain it. While inflation has declined from its 2022 peak, structural factors such as high fiscal deficits, ageing workforces and geopolitical fragmentation increase the risk it will stay high relative to the QE era, potentially limiting the flexibility of central banks. In addition, the growing realization that our planet is facing some significant biophysical constraints means that whatever growth we experience over the next few decades is likely to be shaped in part by those limits. All things considered, financial-market participants could now face higher volatility and shorter business cycles than they have become accustomed to.

In this new regime, we are also seeing increasing divergence in global growth. Notably, the US economy has experienced persistently strong GDP growth, benefiting from its domestic energy sources, large fiscal stimulus and innovation in its technology sector. Europe has struggled as it has had to contend with (until recently) higher energy costs, combined with a lack of innovation. China, meanwhile, has continued to work through the legacy issues related to the crisis in its property sector. Heavy investment in its manufacturing base has given it an edge in the production of electric vehicles and renewable-energy infrastructure. Monetary-policy divergence is another trend. The European Central Bank, for example, recently began to lower borrowing costs ahead of its US and UK counterparts. Such regional variations in the outlook can create opportunities for discerning investors.

Reimagining the Multi-Asset Portfolio

For many asset owners, this very different regime is leading to an urgent review of their investment approach. The QE era has ended and, with it, the ‘long any risky asset’ strategy may have ended too. Given high cash rates, we do not expect the current regime to reward equity market beta in the same way as occurred during the QE era. Similarly, we expect bonds to offer a lower premium, and perhaps more significantly, we already expect bonds to provide a less reliable diversification benefit versus equities. In a macro regime where not only growth but also inflation drives asset prices, the correlation between bonds and equities can turn positive, as we witnessed in 2022. This is a reminder of how things used to be in the pre-QE era of the 1990s and 2000s. Clients may also be contending with a significant portion of their assets being tied up in private markets that lack liquidity and may face markdowns, meaning they could underperform assumptions in their forecasts, and, importantly, lack flexibility to weather the next storm.

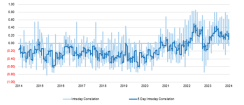

Bonds’ Role as a Diversifier May Be Less Reliable

Intra-day correlation S&P 500® vs. 10-year US Treasury note from 2014-2024

Against this differentiated background of high cash rates and lower premiums, an investment approach founded on ever-rising markets and lower interest rates may no longer reliably deliver the returns clients are seeking. Investors are increasingly looking for returns that do not rely on trending markets, which reaffirms the case for an active, discerning approach to equity, bond and alternatives investing. Moreover, portfolios will need to be reimagined to allocate capital more efficiently, embrace flexibility, and better embed diversification through broader risk management.

Many asset owners have recently been adopting what has been termed a ‘total portfolio approach’, with investment goals that focus less on measuring the performance of individual components versus index-based benchmarks and more on seeking solutions that can contribute to a total portfolio outcome. Often asset owners will have a risk budget and will seek to determine which ‘best ideas’ to allocate it to.

A Liquid Alternative

In this context, we believe that liquid diversifiers could provide investors with a significant opportunity. Liquid and flexible alternative strategies offer the potential for uncorrelated returns and downside risk management, without the high fees and additional risks associated with alternative vehicles.

Relevant components could include:

- Global macro

- Cross-asset trend/managed futures

- Commodity, currency, and rates alpha

- Alternative risk premia

- Equity market neutral

- Tail-risk hedging

The Case for Liquid Alternatives

Different market conditions warrant a different approach

As asset owners have expanded their target allocation to diversifiers and alternative investments, investing in market-neutral, multi-strategy solutions can allow them to gain efficient access to these varied and liquid approaches in a way that we think will be valuable in the new market regime. Even in areas such as wealth management and defined contribution (DC) pensions, which have typically pursued more ‘vanilla’ investment approaches, we have seen an increasing desire to add exposure to liquid alternatives.

Rigorously Fundamental

In this context, and as asset owners embrace total-portfolio approaches, we believe there are knowledge, skills and capabilities that asset managers need to be willing to share more openly. At Newton, we have a strong heritage in delivering both fundamental and systematic multi-asset strategies, with capabilities across equities, fixed income, currencies, commodities and other liquid alternatives.

Since our fundamental and systematic investors started working together following Newton’s integration of Mellon Investments Corporation’s multi-asset business in 2021, our fundamental portfolio managers have been able to improve their own models by harnessing the insights from their systematic colleagues. This has allowed greater efficiency to filter through and has given our fundamental portfolio managers more time to focus on new ideas. For our systematic team, having fundamental colleagues highlighting when trends are about to change can help them de-emphasize certain signals, structure portfolios better, and respond more quickly to a change in direction. Ultimately, clients will look to benefit from the best combination of tools to inform both approaches.

Newton’s Depth of Multi-Asset Capabilities

For investors seeking a straightforward and disciplined approach to diversification, our fundamental multi-asset strategies seek to add value through active, engaged investment. They span income, moderate, balanced and growth outcomes, with security selection driven by our multidimensional research. In addition, our recently launched FutureLegacy range of sustainably managed, risk-rated multi-asset portfolios for the UK DC market combine the expertise of multiple investment desks and encompass strategic and tactical asset allocation.

Newton also has a long track record in providing absolute-return solutions that can invest in a range of asset classes and use simple hedging strategies to manage risk, providing investors with the potential to enjoy attractive long-term total returns. These portfolios include our established Global Real Return and Global Dynamic Bond strategies, which seek to deliver risk-adjusted absolute returns over the long term.

Our discretionary offerings are complemented by a range of fundamentally driven strategies that are systematically delivered, spanning ‘better beta’, benchmark-relative and overlay, and absolute-return capabilities. The systematic team has a 40+ year heritage with expertise that spans alpha generation (via trend, macro and relative value components) and better beta portfolio building blocks through a disciplined and repeatable process. While based on a systematic investment process, active investment decisions are fundamentally driven in a macro and risk-aware framework.

Multi-Strategy Solutions

Building on these multidimensional capabilities, and deconstructing the underlying building blocks, we have been working actively on how we can combine our ‘best ideas’ and alpha sources into a range of multi-strategy solutions that seek to deliver the best possible risk-adjusted outcomes for each client in the environment we are in. In doing so, we’re committed to offering solutions that are transparent, offer liquidity, have an attractive fee, and align our interests with those of our clients.

Expert Partnership for the New Market Regime

Beyond managing their investment portfolios, many asset owners are at ‘peak busy’ as they embrace technological innovation and manage day-to-day governance, regulation and talent – all of which are becoming increasingly complex, especially as more capabilities are insourced. This has major implications for asset managers, as asset owners are likely to want fewer and deeper manager relationships. In this context, asset managers must rethink how to be a better expert partner to help meet clients’ specific goals. It will be critical to deeply understand clients’ requirements, offer building blocks that can complement their internal and external allocations, transfer knowledge openly, and innovate collaboratively in terms of the development of new solutions.

When we think about how we can unlock opportunity for our clients, we see the starting point not as a benchmark, but as each individual client’s goals and challenges. If we properly understand the context our clients face, we believe we can deliver the outcomes that allow them to get to the right place. This is at the heart of how we at Newton set out our ambition to be the most admired asset manager, as a valued strategic partner to those on the journey to becoming the most admired asset owners.

Mitesh Sheth, FIA, MBE

Multi-Asset Chief Investment Officer

Mitesh has oversight of Newton’s multi-asset and fixed-income teams based in London, as well as Newton’s quantitative multi-asset solutions team in San Francisco.

Important Information

For Institutional Clients Only. Issued by Newton Investment Management North America LLC ("NIMNA" or the "Firm"). NIMNA is a registered investment adviser with the US Securities and Exchange Commission (“SEC”) and subsidiary of The Bank of New York Mellon Corporation (“BNY Mellon”). The Firm was established in 2021 and is part of the group of affiliated companies that individually or collectively provide investment advisory services under the brand “Newton” or “Newton Investment Management”. Newton currently includes NIMNA and Newton Investment Management Ltd. (“NIM”) and Newton Investment Management Japan Limited (“NIMJ”).

Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell investments in those securities, countries or sectors.

This material is provided for general information only and should not be construed as investment advice or a recommendation. You should consult with your advisor to determine whether any particular investment strategy is appropriate. Statements are current as of the date of the material only. Any forward-looking statements speak only as of the date they are made, and are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Past results are not indicative of future performance and are no guarantee that losses will not occur in the future.

The indices referred to herein are used for comparative and informational purposes only and have been selected because they are generally considered to be representative of certain markets. Comparisons to indices as benchmarks have limitations because indices have volatility and other material characteristics that may differ from the portfolio, investment or hedge to which they are compared. The providers of the indices referred to herein are not affiliated with NIMNA, do not endorse, sponsor, sell or promote the investment strategies or products mentioned herein and they make no representation regarding the advisability of investing in the products and strategies described herein.

Some information contained herein has been obtained from third-party sources that are believed to be reliable, but the information has not been independently verified by Newton. Newton makes no representations as to the accuracy or the completeness of such information and has no obligation to revise or update any statement herein for any reason. Charts and graphs herein are provided as illustrations only and are not meant to be guarantees of any return. The illustrations are based upon certain assumptions that may or may not turn out to be true.

MAR006488 Exp 08/2025.