This blog is part of a new series on Institutionalinvestor.com entitled Global Market Thought Leaders , a platform that provides analysis, commentary, and insight into the global markets and economy from the researchers and risk takers at premier financial institutions. Our first contributor in this new section of Institutionalinvestor.com is AllianceBernstein, who will be providing analysis and insight into equities.

Feast or famine: The easy lending that contributed to the 2007–2008 financial crisis gave way to a closing of the credit spigot to just a drip. Newly conservative lending institutions remained stingy despite massive government efforts over the past couple of years to pump liquidity into the financial system. In the end, relatively little of this capital found its way into borrowers’ pockets.

This would hardly seem to be an attractive backdrop for investing in banks. But in our view, it may be just the time, as much has been quietly changing in the background in the past several quarters.

Perhaps most important, consumers have been repairing their balance sheets. The household obligations ratio, which measures how much disposable income is used to cover household debt as well as related taxes and insurance, has been running at its lowest levels since the mid-1990s. This reflects a vast improvement in households’ creditworthiness in just the past three years.

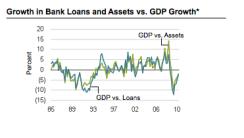

And while loan growth for the 2010 calendar year ranked among the lowest on record, that statistic masked a return to positive growth in the fourth quarter—the first quarterly increase in two years. Although loan growth was sluggish in 2011’s first quarter, due to typical seasonal effects, we remain positive on the outlook for the rest of the year.

Although there is great variability among institutions, we see the credit landscape today as a potentially fertile source of opportunities. Large banks' return on assets has been recovering strongly—even touching record levels when recent increases in loan-loss provisions are put aside—yet valuations are extremely attractive. Recent share prices for an aggregation of leading banking institutions imply that, for at least the foreseeable future, these companies’ return on equity will see little or no rebound from 2010’s historically depressed levels. Yet a number of institutions have been enjoying steadily rising consensus earnings forecasts because of improving credit outlooks, in sharp contrast to the negative industry view that has been driving stock prices.

* Through May 31, 2011. Growth rates in assets or in loans minus growth rate in nominal GDP. Positive numbers indicate the metrics grew faster than GDP.

Source: FactSet, FDIC, US Bureau of Economic Analysis, Factset and AllianceBernstein

Scott Wallace is the Team Leader—US Large Cap Growth at AllianceBernstein

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio management teams.