This blog is part of a new series on Institutional Investor entitled Global Market Thought Leaders, a platform that provides analysis, commentary, and insight into the global markets and economy from the researchers and risk takers at premier financial institutions. Our first contributor in this new section of Institutionalinvestor.com is Alliance Bernstein, who will be providing analysis and insight into equities.

Not a week goes by without a corporate defined benefit plan sponsor telling me that he or she needs to be more conservative. Under new pension accounting rules, the wild market volatility of recent years has led to huge swings in plans’ funded status—and thus, unexpected (and unwelcome) calls for employer contributions.

“We just can’t stay at 60% equities,” one plan sponsor told me. “We’ve simply got to cut our equity allocation—maybe to 30%.”

I understand the feeling. But a lower equity allocation isn’t always more conservative. Today, lower equity allocations would likely compound a plan’s problems.

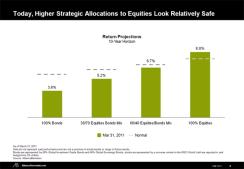

Consider our most recent 10-year return projections for equities, bonds and two simple asset allocations: a 60/40 and a 30/70 mix of equities and bonds (Display). Our research into the fundamental building blocks of asset-class returns and their likely interactions allows us to forecast the “normal” range of outcomes, as well as the most likely range of outcomes under current conditions. Of course, these are projections; there’s no guarantee that any portfolio will actually perform this way.

For global large-cap equities, our current 10-year median annualized return projection is 8.8%, well above our normal median projection of 7.9% for the same period. Equity valuations are normal, so multiple expansion isn’t driving our above-normal current projection. With volatility close to normal, our strong equity-return projection primarily reflects strong global corporate profitability and slightly above-average dividends.

For a global diversified-bond portfolio hedged to and reported in US dollars, our current 10-year median annualized return projection is 3.6%, far below our normal median projection of 5.8%. In normal times, we would see less than a one-in-10 chance of 10-year bond returns being so low.

Our current projections for bonds are low because global sovereign-bond yields must rise eventually from current depressed levels. And the downward pressure on bond returns from rising sovereign yields would swamp the projected gain from narrowing credit spreads—even for a diversified bond portfolio with a 60% allocation in investment-grade credit.

In normal times, cutting the equity weight from 60% to 30% would mean giving up 0.7% in median projected annual returns over 10 years. But in the current environment, it would mean giving up 1.5%—more than twice as much.

To put this in perspective, we now project that $100 invested in the 60/40 portfolio would reach a median value of $191 after 10 years, while $100 invested in a 30/70 portfolio would reach $166. For companies worried about having to make large future contributions to their plans, the “conservative” option could be counterproductive. It’s worth thinking twice before reducing exposure to equities.

Note: The projections cited were as of March 31, 2011 and are subject to change.

Seth Masters is Chief Investment Officer—Asset Allocation at AllianceBernstein

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio management teams.