As a key decision maker, you worry: How to recruit and retain talented employees, from ladder-climbing Millennials to mid-career executives. The company that enriches employees’ lives—and their pocketbooks—will earn the loyalty of the high-value personnel who are in such demand.

It’s time to retool your benefit strategy

The challenges of nurturing a multi-generational 21st-century workforce are unrelenting. In a report detailing the top workplace trends in 2016, the Workforce Institute at Kronos notes that many organizations will have to “rethink and retool their benefits strategies to create a competitive advantage in the war for talent.”

In an effort to attract and retain the “the most diverse and multi-generational workforce in history, there will be an emergence of unique benefits that target employees at different stages of their lives,” the report says.

Financial wellness is a primary beachhead when trying to attract top talent. But it goes beyond simple retirement planning and into an expanded view of retirement income—a strategy tailored for every generation, from the savvy Millennial and skeptical GenXer, to the ready-for-what’s-next Baby Boomer.

A solution for today’s employee

Unfortunately, most people aren’t wired to manage their own investments. It isn’t just a lack of know-how; emotions get in our way. Our “fight or flight” instincts simply don’t serve us well in sometimes volatile markets. These instincts can cause us to react to small fluctuations in stock prices—rather than take a step back to understand the benefits of a long-term approach.

Employee retirement plans are built for the long-term investor, not short-term traders who tend to mistime the market by buying at the top of the market and selling at the bottom. Still, when many plans include dozens of investment choices, picking and maintaining the right investment mix can seem daunting. So how should plan participants choose their investments, and how often should they adjust their mix? Target date funds (TDFs) can be the answer.

Faced with a fiduciary mandate, an increasing number of investment advisors are recommending target date funds to meet the needs of a bewildered workforce overwhelmed by so many investment choices.

Not all target date funds are the same

Target date funds can be a prudent and fiduciary-friendly Qualified Default Investment option. An investor nearing retirement with a short-term investment horizon would tend to lead toward potentially less volatile—and generally lower-yielding—investments. A TDF can do this automatically.

Conversely, a Millennial many years from retirement might choose a TDF with mostly equity-driven investments. The common thread is that both types of investors, and those in any generation for that matter, wouldn’t need to worry about adjusting their investment mix over time; the glide path within their TDF will automatically do it for them.

But it’s important to understand that even similarly-dated TDFs aren’t the same. The glide path of each family of target date funds is unique and the equity exposure that is embedded within those glide paths can vary across the same vintage as a result. The asset classes the funds invest in will also differ between TDFs. Some may offer only traditional equity and fixed income options, while others may also include Real Estate Investment Trusts (REITs), commodities, and complicated alternative asset classes, but at different levels in the investment cycle. It is important to consider the underlying equity levels and asset allocation of each TDF to ensure that investors are not taking on too much or too little risk for their life stage. Younger investors would be wise to explore the traditional asset mix of TDFs to ensure they offer enough potential growth, while investors later in the cycle may want a larger mix of lower-risk investments.

Whatever the workforce make-up and investing appetite, plan participants can take comfort in knowing that TDFs offer varied strategies tailored to all phases of retirement saving. TDFs give employees peace of mind and added value in the form of a simple, targeted retirement investment vehicle, making it a useful investment option for today’s workforce.

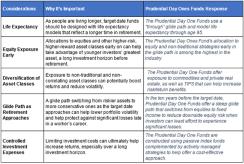

A glide path that addresses risk at all stages

Prudential Day One Funds

The investments in a target date fund typically change as investors get closer to their projected retirement date. This is known as a glide path, in which TDF asset managers work to change a fund’s asset mix over time. But it’s important to keep in mind that not all TDFs are the same.

While a dynamic glide path designed to address risk is the hallmark of any TDF strategy, the various attributes to consider when selecting the right TDF for your plan include:

Find out more by visiting DayOneFunds.com

Investing involves risk. Some investments are riskier than others. The investment return and principal value will fluctuate, and shares, when sold, may be worth more or less than the original cost, and it is possible to lose money. Past performance does not guarantee future results. Asset allocation and diversification do not assure a profit or protect against loss in declining markets.

The target date is the approximate date when investors plan to retire and may begin withdrawing their money. The asset allocation of the target date funds will become more conservative as the target date approaches by lessening the equity exposure and increasing the exposure in fixed income type investments. The principal value of an investment in a target date fund is not guaranteed at any time, including the target date. There is no guarantee that the fund will provide adequate retirement income. A target date fund should not be selected based solely on age or retirement date. Participants should carefully consider the investment objectives, risks, charges, and expenses of any fund before investing. Funds are not guaranteed investments, and the stated asset allocation may be subject to change. It is possible to lose money by investing in securities, including losses near and following retirement.

Prudential Day One Funds are offered in the following structures: (i) separate accounts available under group variable annuity contracts issued by Prudential Retirement Insurance and Annuity Company (PRIAC), Hartford, CT, a Prudential Financial company (ii) collective investment trust funds established by Prudential Trust Company, as trustee, a Pennsylvania Trust Company located in Scranton PA, and a Prudential Financial company. Each of PRIAC and Prudential Trust Company is solely responsible for its own contractual obligations and financial condition. Offers of the collective investment trust funds may only be made by sales officers of Prudential Trust Company.

A target date fund should not be selected based solely on age or retirement date, is not a guaranteed investment and the stated asset allocation may be subject to change.

The Day One Funds, as insurance company separate accounts or collective investment trust funds, are investment vehicles available only to qualified retirement plans, such as 401(k) plans and government plans, and their participants. Unlike mutual funds, the Day One Funds are exempt from federal securities laws and not entitled to the protections of those laws. They are instead subject to regulation under applicable bank or insurance laws.

© 2016 Prudential Financial, Inc. and its related entities. Prudential, the Prudential logo, the Rock symbol, and Bring Your Challenges are service marks of Prudential Financial, Inc., and its related entities, registered in many jurisdictions worldwide.

0293780-00001-00