The belief that passive investing is risk-free is a misconception, in our view at AllianceBernstein. Whereas passive portfolios may address concerns about relative risk, they won’t help investors mitigate absolute risk when markets decline and may leave investors exposed to market bubbles and distortions. And by choosing a purely passive approach, an investor will forgo any potential for additional returns when it matters most — in an era in which market performance is likely to be subdued.

In recent years, heavy fund flows into passive portfolios have reflected the growing belief that active management cannot be relied on for outperformance. Although it’s true that even skilled active managers will not outperform every year, many have demonstrated an ability to do so over time.

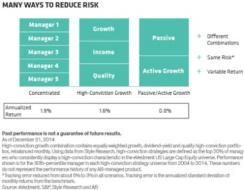

Our research has identified U.S. large-cap equity managers who demonstrated conviction in various ways. We then looked at how combinations of these high-conviction equity managers performed in an equity allocation. We found that there are many different ways to reduce risk.

The three examples shown in the illustration (see chart 1) below demonstrate different approaches to achieving the same amount of relative risk. In the first two cases, we found that risk could be reduced to similar levels — from about a 6 percent tracking error to 3 percent — by combining five concentrated equity managers or by putting together a package of three different types of high-conviction managers with diverse characteristics.

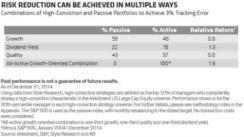

By combining passive and high-conviction portfolios with diversifying characteristics, we found that investors can reduce tracking error substantially, compared with a purely active single-manager option, while also enjoying better returns than the benchmark provides before fees (see chart 2).

Different types of investing strategies require different mixes of passive and active allocations to reduce risk effectively. Creating a growth allocation that is 55 percent passive and 45 percent active would cut tracking error from 6.6 percent to 3 percent for a 100 percent active growth strategy while still delivering above-benchmark returns. In a dividend yield approach, it would take a 22 percent passive allocation to achieve a similar result. By contrast, an all-active mix with a growth-oriented combination could create an allocation with a similar risk profile but higher returns.

Of course, there are many things to consider before choosing the right approach for individual needs. For starters, fee budgets may determine how much is available to allocate to active strategies. Yet there is a trade-off between the additional cost of fees for skilled high-conviction active managers and the risk reduction achieved in cheaper, passive portfolios. As the chart shows, the all-active combination delivered an annualized relative return of 1.6 — about twice the return of the active growth and passive combination. In other words, the all-active combination delivered an 81-basis-point advantage, which should be compared with the incremental fees of having a 55 percent greater allocation to active managers.

Additional considerations include an investor’s philosophy about different approaches to the markets. Manager selection risk adds further uncertainty. If you can identify an active manager who is capable of consistently beating the benchmark after fees, then we believe it’s preferable to stay active and forgo passive strategies. But armed with an understanding of how passive and active approaches work together, investors can address the many considerations related to manager selection with the right mix of strategies.

To make an equity allocation work harder, the portfolios that you pick matter. Much depends on how much active risk you can tolerate. We believe that combining different high-conviction strategies — or combining active and passive strategies — can help investors ensure that money spent on active management is deployed appropriately for their individual goals.

Dianne Lob is senior managing director for equities, and Nelson Yu is head of equities quantitative research; both at AllianceBernstein in New York.

See AllianceBernstein’s disclaimer.

Get more on equities.