European high-yield is the brightest spot in global credit at the moment. Here is but a handful of reasons why.

First, the so-called credit clock is still favorable. Simply put, European high-yield is at a more benign place in the credit cycle than its U.S. counterpart. It stands to benefit from the ongoing improvement in European corporate earnings and minimal exposure to the struggling energy and mining sectors. The weak euro and low commodity prices benefit the more consumer-oriented composition of the European high-yield market. As European banks continue to restructure, with bank lending conditions easing and demand for bank loans increasing, this should in turn help support corporate credit quality and growth prospects. Meanwhile, shareholder-friendly — that is, creditor-unfriendly — activity such as share buybacks and debt-funded M&A in Europe remains well below U.S. levels and the levels achieved at the peak of the last credit cycle, in the mid-2000s. Monetary policy is also a plus: The Federal Reserve has begun its long-awaited tightening cycle, whereas the European Central Bank continues to loosen policy.

Second, the constrained supply of European high-yield is supporting its value. The credit quality of new debt issuance has been solid, and the expected net supply will most likely fall again in 2016 as more borrowers opt for the leveraged loan market. In other words, investor demand has a higher probability of outpacing the growth of the market. At the same time, ECB quantitative easing continues to shrink the available universe of fixed-income investments that produce a positive yield.

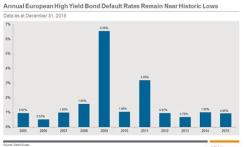

Third, European high-yield default rates remain very low (see chart), meaning that investors are well compensated for buying riskier credit. Defaults averaged below 1 percent in 2015. We at J.P. Morgan Asset Management expect that rate to remain comfortably below 2 percent throughout 2016, a level that is already priced into the market. Credit spreads are essentially pricing in a multiple of where default rates should be, creating an attractive cushion.

Fourth, European high-yield remains relatively insulated from struggling commodity sectors, when compared with the U.S. high-yield market, which has more significant vulnerability. Whereas troubled sectors account for as much as one third of the U.S. index, they make up just 3 percent of its counterpart in Europe.

Finally, the strong underlying credit quality in European high-yield provides a powerful fundamental backdrop. The sector is experiencing a trend of credit upgrades, with companies such as Lufthansa, Telekom Austria, Groupe Renault, EDP and Lafarge being promoted out of the benchmark and into investment-grade status. The number of rising stars has outpaced that of so-called falling angels — companies getting downgraded into high-yield.

Peter Aspbury is a portfolio manager and head of European high-yield strategies at J.P. Morgan Asset Management in London.

See J.P. Morgan Asset Management’s disclaimer.

Get more on fixed income.