Having an affinity for both asset-backed securities and hit pop songs, the 2014 Meghan Trainor song “All about that Bass” is a perfect melodic metaphor for how we look for value in today’s late market cycle. Within securitized assets - in particular, the commercial real estate or “CRE” space – we think investors shouldn’t reach for yield given today’s expensive levels. Therefore, finding properties that offer lower, i.e. more attractive, loan-to-value ratios and with lower costs basis makes a lot of sense.

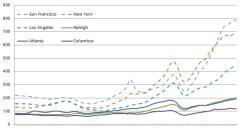

To illustrate this point, consider the current valuations in the “Big Six” cities (New York, San Francisco, Los Angeles, Boston, Chicago, and Washington DC). These cities have seen particularly aggressive capital provision, driving up values and increasing the property and loan cost basis. These are the cities which are internationally known, but anyone leasing or renting in these areas knows how expensive they can be. At the same time, property values in other major cities such as Raleigh, Atlanta and Columbus haven’t increased as quickly, even though fundamentals, such as occupancy, rent growth, and supply/demand dynamics in those markets can be as strong (if not stronger) than the fundamentals seen in the Big Six. This is an extremely important point.

Figure 1: Commercial Real Estate comparisons: How smaller big cities compare to the Big Six

Source: Schroders, CoStar, March 2018. Not intended to be a comprehensive listing of markets.

A low cost basis in a property not only enables equity owners to enjoy greater margins when rents are rising, but it also offers a level of protection in the event property values are declining. From a lending perspective, that’s a beautiful proposition, since a low basis provides a compelling competitive advantage. The lower the rent, the larger the tenant pool, which can help to maintain occupancy, preserve cash flow, and provides a cushion to enable debt service coverage in a downturn.

One way to get access to property with a low cost basis is by lending to borrowers whose properties have recently seen a basis “reset”. An example might be properties bought with bridge loans, which are short-term (3-5 year) loans that often finance an acquisition of a property that is underperforming its local market. It’s important to note that accessing these investment opportunities is not easy; it requires sourcing and servicing ability – so don’t try this at home.

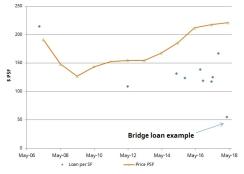

The below illustration of a property in West Palm Beach, Florida, shows the importance of the cost basis, using collateralized mortgage backed securities (CMBS) data. The greater Palm Beach area is well known, not least for being home to Mar-a-lago, a club belonging to the current US President. Even so, the area is not as well known as a New York or Los Angeles, and doesn’t attract the same foreign investment. The orange line represents the historical median price per-square-foot (PSF). It is easy to see the more than 30% decline experienced during the Global Financial Crisis (GFC).

The blue diamonds, on the other hand, represent the actual loan per square foot for individual properties in the CMBS market. Notably, by lending, the investor has picked up a comfortable cushion to stressed conditions, even to the GFC. Most of the blue diamonds (the loan per square foot) remain lower than the median price per square foot during the GFC. Furthermore, a look at smaller loans indicates that the price PSF and loan PSF figures are even lower than the median. This represents a healthy margin of safety.

Figure 2. Many regions offer bridge loan PSF levels that are remarkably lower than GFC era – West Palm Beach Office Properties example

Source: Trepp, CoStar, Schroders through May 2018. For illustration only. Loan values and prices are subject to change, and can vary loan to loan.

For further illustration, we have indicated the cost basis and the loan basis for a bridge loan in the same city. While the city as a whole has average loan balances of $140 PSF and average valuations of $220 PSF, this particular bridge loan has a $55 PSF loan basis to facilitate an acquisition of a property with a $74 PSF basis. This bridge loan creates an attractive proposition, with an inherently defensive posture in the event of a near-term market downturn.

No trouble – why investors should be defensive in the CRE market

Historically low levels of interest rates, low yields, and reduced expected returns have sent global investors in search of more return, yield, and/or income. As a result many have large overweights to credit or to equities. The CMBS market is another area where risk-seeking behavior can be seen. The CMBS credit curve, or the yield spread difference between securities rated AAA and those rated BBB- (triple-B minus), is currently at the lowest level seen since 2009. In other words, trying to earn more income when the credit curve is flat has forced investors further down the capital “stack”, when they are least compensated to do so. We think now is the point when investors should be rotating into investments with more stability or a greater margin of safety, given compensation for taking on greater credit risk is lower.Conclusion

By exploiting lending inefficiencies in the private CRE loans market, an investor can pursue higher return and more protection from a downturn in the economy and/or real estate market values. Risk/return profiles can be enhanced by targeting less crowded, less glamorous real estate loans. By virtue of lower competition, property valuations are more reasonable and a lower loan PSF is available.Lending in cities like Jacksonville, Dallas, or Charleston, SC, to name a few, reduces competition and can offer the potential to achieve a higher return, while providing downside protection through a lower cost basis. Smaller CRE loans have not been targeted by the massive amount of global QE capital. But for those with the ability to properly source them, investing in a well-diversified portfolio of these loans can be an attractive way to earn a stable return profile over a 3-5 year period, effectively addressing a challenging investment environment by capitalizing on inefficiency.

In short, it’s all about that basis, no trouble.

Read more Schroders thought leadership