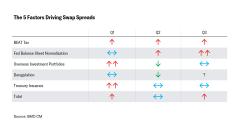

Where will spreads go next?

Five key factors that we believe have been the primary drivers behind the increase in Libor/swap spreads in Q1 are outlined in the box below, as well as our expectation for the pressure they will exert both in Q2 and the longer term.

When taken together, our five factors paint a stable picture for Libor. However, given the magnitude of the Q1 move, we believe that even a stable environment for Libor will likely coincide with some declines in Libor/OIS and swap spreads. We attempt to take advantage of this sentiment with our current trade recommendations.

However, the long-term picture for Libor and swap spreads remains higher, and we recommend setting trades with short (three month) time horizons and narrow targets. Here’s the rationale behind our expectations for Libor/swap spreads in both the second quarter and the long term.

Inter-affiliate tax adds to Libor/OIS BEATing

In addition to repatriation of overseas investment portfolios, the U.S. tax reform included another measure that has a significant impact on Libor: the Base Erosion and Anti-Abuse Tax (BEAT). In a nutshell, the BEAT tax is Uncle Sam’s attempt to capture taxes on multinational firms that could historically avoid taxes through transfer payments to foreign affiliates.

This tax has a large consequence on inter-affiliate money transfers such as those foreign banks use to fund foreign branches in the U.S. In an attempt to avoid the BEAT tax, foreign banks are incentivized to have their U.S. branches issue unsecured debt in the U.S. rather than relying on funding them directly through inter-affiliate transfers.

This phenomenon potentially explains how Libor/OIS has widened so dramatically with very little reaction in cross currency bases. If this is the case, then as the debt that was originally issued to fund U.S. branches matures, excess dollar reserves in the financial system will decline. As excess liquidity declines, dollars become dearer, influencing Libor higher. This aspect of BEAT is especially concerning when viewed in conjunction with our next factor on Libor/OIS: Fed balance sheet normalization.

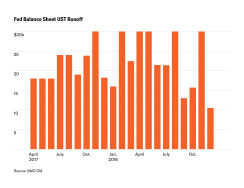

Fed Balance Sheet Normalization Will Add Pressure Later this Year

Libor’s recent rise has been largely credited to bill issuance, repatriation flows, and even other aspects of the tax reform, but the normalization of the Fed’s balance sheet is poised to become a very significant driver in funding going forward.

The chart below shows the amount of Treasury securities the Fed plans to allow to mature without reinvesting through 2019. Through the end of March, the Fed’s caps had been met for each month with respect to maturing Treasuries, and its Treasury portfolio declined by $54 billion over the first six months of its balance sheet runoff program.

As the caps increase each quarter, the amount of USD reserve assets drained from the system will be allowed to grow. We estimate that $193 billion in Treasuries will roll off the Fed’s portfolio in the second through fourth quarters of 2018. Further into the future, an additional $270 billion should roll off in 2019.

As the Fed drains USD reserve assets from the banking system, the supply of dollar funding contracts. Measuring this by the monetary base, we can estimate the impact of a reduction in reserves on market stress.

Repatriation flows likely slowing

Perhaps the most impactful flow – and certainly the least quantifiable – is the repatriation of foreign earnings. The market will get some insight into these moves in coming months as first quarter financials are released. Generally, corporations with earnings booked abroad held a mixture of short-dated Treasury, agency, and corporate debt; the winding down of these portfolios will increase private borrowing costs.

We suspect the corporate portfolios will shrink by some combination of selling assets and allowing the debt to gradually mature. As there is no obvious incentive to delay the selling of debt, it is highly likely that corporations electing to sell debt outright did the vast majority of selling in the first quarter.

With the caveat that we will have limited insight into the flows from these corporate portfolios, we expect the repatriation flows to subside in the medium-term. Of course, the portfolios that are intended to be run down gradually will result in a prolonged reduction in demand for a variety of debt. However, the rash of selling likely took place in the first quarter, and funding should see some relief in the near-term.

We continue to expect that first quarter financials for corporations with the largest foreign earning portfolios will reveal plans for significant share repurchases and dividend payments.

T-bill issuance to provide some near-term Libor relief

We expect the paydown in T-bills to provide some downward pressure on Libor and GC, which should help stem Libor’s rise as the crowding impact of T-bill issuance fades. Q2 net issuance should be about flat after T-bill supply jumped 18% in the first quarter, acting as a massive front-end swap spread widener that crowded out private sector borrowers. In such dramatic moves in issuance, the impact on Libor outweighs the impact on repo.

However, Libor has not historically been motivated by relatively smaller changes in T-bills. We expect the mild downward pressure on Libor to be counterbalanced by a decline in repo rates, which works to widen swap spreads. Taken together, this presents a balanced outlook on swap spreads for Q2, but at least the significant widening pressure experienced during Q1 will fade. In the long term, we expect these forces to continuing offsetting each other, resulting in a stable Treasury issuance related impact on swap spreads in the long term as well.