Click here to download a PDF of the full report.

While many fixed-income investors are still chasing yield, others are focused on managing risk exposures, reducing volatility, and preserving capital.

“The financial market is undergoing a cyclical uptick, but there are serious structural headwinds — slow economic growth, high debt levels, geopolitical tensions and the long-running bull market,” says William J. Adams, CIO — Global Fixed Income, MFS Investment Management. “We believe valuations in the fixed-income market may not reflect these risk factors.”

Noting that fixed income traditionally plays a balancing role in a diversified portfolio, Adams adds, “In an environment where spreads appear particularly tight, it is important to keep this key function in mind and manage fixed income with the appropriate prudence. Rather than pursuing their quest for higher yields, institutional investors should focus on preserving capital through active risk management — a strategy that is well-suited for today’s uncertain market environment.”

Those uncertainties include global central banks retreating from quantitative easing (QE), economic stagnation, high debt levels, adverse demographic trends, political dysfunction, geopolitical tensions and technology dislocations, says Adams. “The focus of fixed income should be on prudent capital preservation, given the host of factors weighing on the global economy and the aging business cycle.”

A changing world

Since the financial crisis, central banks have provided a relatively stable, low-rate environment for fixed-income investors. “This unprecedented support has helped maintain generally low market volatility and rewarded broad risk-taking,” says Scott Mather, CIO, U.S. Core Strategies, PIMCO.

With conditions favorable, investors have poured far more into fixed-income than equities, says Emily Roland, Head of Capital Markets Research, John Hancock Investments. “The flow into the fixed-income market in recent years has been extraordinary,” she says. “In fact, more than $300 billion has been invested in fixed income funds and exchange-traded funds (ETFs) this year. It remains to be seen if this seemingly insatiable demand for fixed income can continue as central banks around the world march down the path of rate normalization.”

With the re-emergence of global growth, Roland expects the Fed to continue its slow and steady rate increases. “That will be a challenge to the interest-rate sensitive parts of the fixed-income market,” she adds. “However, the move should be an orderly one, and we don’t expect a significant drawdown in fixed income.”

In the investment-grade sector, investors can benefit from a reasonable balance between potential returns and diversification benefits, says Roland. Other areas of the credit markets may offer higher yield, but their correlations to equities are higher, she adds.

Mather suggests considering high-quality Treasury exposure, although only in intermediate maturities since front-end maturities are less attractive with the Fed increasing rates. He adds, “With global central banks adopting less accommodative stances, we prefer interest rate exposure within the U.S., relative to interest rate exposure outside the U.S.”

Looking at durations, Adams says investors may not find many alpha opportunities in the rate structure. “While there is no immediate need for investors to adjust their current duration profiles, we would not suggest increasing those allocations and placing a big bet on going long,” he adds.

A focus on quality

Strong interest in corporate debt has driven up the price of corporate bonds — and led to spreads tightening in both investment grade (IG) and high-yield (HY) debt, according to a recent white paper, “Live to Fight Another Day: Capital Preservation Is Key in Fixed Income Today,” by Adams and James Swanson, Chief Investment Strategist, MFS.

In the pursuit of yield, investors have also rushed to buy equities that serve as bond proxies — utilities, telecommunication stocks, and real estate investment trusts (REITs), for instance — leading to high prices and low dividend yields for these securities. “Investors would be well placed to focus on broadening the opportunity set, actively selecting securities, allowing for flexible allocations where appropriate, and constructing portfolios with prudent risk management controls to ensure adequate compensation for risk,” say Adams and Swanson

In a market with tight spreads, there is less dispersion between lower-quality and higher-quality assets in the various fixed-income sectors. Therefore, Adams suggests that institutional investors look for opportunities to improve the quality of their fixed-income holdings, whether in the investment grade or high-yield sectors.

For instance, one active strategy in the high-yield sector would be to shift money from CCC-rated bonds into the Bs and BBs, Adams says. Those higher-rated credits are less likely to have drawdowns in a more challenging market environment, he adds.

“The same strategy can be applied to the investment grade portion of a fixed-income portfolio,” Adams says. “Moving up the quality spectrum may reduce the number of yield opportunities, but if the markets weaken, investors are less likely to be faced with a sell-off situation. If there is a market decline, they can then decide to reengage and pick up lower-rated securities at significantly lower prices.”

Adams adds, “The greatest determinant of future returns in fixed income is the price you pay today. Since the risk premiums are being squeezed out of market, those future returns look stretched as well. We suggest a cautious approach, and reducing your exposure to the more volatile fixed-income asset classes.”

Seeking yield opportunities

Fixed-income investors seeking higher yields may need to take a tactical approach to the credit market and perhaps broaden their opportunity sets.

“Valuations on emerging market debt are relatively attractive compared with high-yield bonds,” says Roland. “HY has held a spread premium over emerging market debt for an extended period, but that premium has declined and is very small today. When the spread differential between the two is so narrow, historically emerging market debt has outperformed HY in subsequent periods.”

Mather believes there are still relative value opportunities throughout the market. In corporate bonds, for instance, investors might consider the financial sector because balance sheets and spread levels are attractive.

“We also favor other diversified sources of yield, including non-agency mortgage-backed securities, which offer attractive fundamentals and compelling yields,” says Mather, adding that the underlying borrower profile for these legacy securities is improving with lower loan-to-value ratios.

“Given the later stage of the corporate credit cycle, we are focusing on bottom-up credit opportunities and emphasizing portfolio liquidity,” Mather adds. “This includes sector and credit assessments for better fundamentals, stronger asset coverage, and potential for organic de-leveraging.”

Roland notes that the unwinding of the Fed’s balance sheet will also affect the mortgage-backed securities (MBS) market. The Fed holds nearly $2 trillion in MBS, and no one knows if there is enough pent-up demand in the market to pick up the slack, she says.

Adams says there are still some opportunities in structured credits, such as commercial mortgage-backed securities (CMBS) and collateralized loan obligations (CLOs). “But investors need to do their research and be very selective,” he says. “Every security should be vetted and understood before adding it to a fixed-income portfolio.”

In the municipal bond market, Adams does not expect Puerto Rico’s debt problems to carry over to other issuers. “If the tax advantages of munis make sense to an investor, we see no reason to exit this asset class,” he says. “We do, however, suggest looking at the quality of your current holdings and remaining prudent with your risk exposures.”

Outside the U.S., dislocations in the markets may create opportunities. “We view Japanese interest rates as a great vehicle for hedging exposure to U.S. interest rates,” says Mather. “The likelihood of bond yields falling in Japan is quite low, while there are several scenarios in which yields could move higher.”

In emerging markets, sovereign and corporate debt can provide compelling value at times. But investors should be clear about which risk factors, such as local interest rates, currency or credit, may be attractive at any particular point. “We focus on healthier balance sheets and solid fundamentals, while remaining mindful of any potential shifts in the broader macro landscape that could affect emerging markets,” Mather says.

Active or passive strategies?

Whether seeking yield or managing risk, fixed-income investors may benefit from active strategies tailored to their objectives.

“Investors would be wise to focus on risk management by engaging in active security selection,” Adams says. “While we are not proponents of tactically trading asset classes, we do believe that active risk management is vital in today’s market. Specific security selections by your asset manager can make a difference in your risk-adjusted returns.”

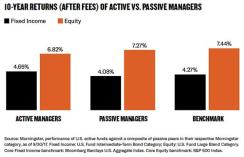

Drilling into the issue of active versus passive strategies, Mather says there are significant differences between managerial performance in the equity and fixed-income sectors.

“If you examine some of the largest equity categories over the past 10 years, the median active manager has underperformed both its benchmark and the median passive provider,” Mather says. “However, the same is not true for fixed income, where the median active manager has outperformed the median passive peer in the largest fixed income category by more than 0.5 percent per year for the past 10 years after fees. If you look at the top quartile managers, you can see consistent excess returns of about 1 percent per year.”

Why the difference? Mather says active managers can exploit structural inefficiencies in the bond markets. One reason is that a large portion of the $100+ trillion fixed income-market is held by central banks, insurers, and other financial institutions that may not prioritize maximizing returns.

“That allows active managers to take advantage of dislocations and mispricings,” Mather says.

Avoiding complacency

Looking toward the new year, Mather says investors should review their fixed-income strategies with a goal of reducing correlations to risk assets.

“A period of low volatility helped by years of unprecedented central bank support has lulled investors into only focusing on return and yield at the expense of diversification and balance in portfolios,” he says. “We think this is an environment where institutional investors should truly focus on diversification and capital preservation, since return of capital may prove more important than return on capital.”

As Mather says, a strong diversifier for risk assets such as equities is a true core bond strategy — a high-quality, diversified portfolio that can provide resilient return streams when adverse market conditions affect riskier assets.

— Richard Westlund