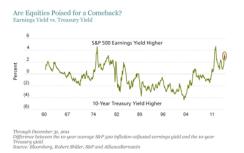

Investors remain wary of equities. For many, stock valuations, while attractive versus history, still don’t seem compelling enough to compensate for the extreme uncertainties in the world today. But investing is also about comparative opportunity cost. From that perspective, one fairly predictive metric we follow suggests that the opportunity in equities has rarely been as provocative as it is now. I’m talking about the yawning gap between the stock market’s earnings yield (the reciprocal of its price/earnings multiple) and long-dated government bond yields.

Our ‘yield gap’ compares an inflation-adjusted earnings yield (based on 10-year average trailing earnings, to normalize business-cycle gyrations) to the nominal yield on 10-year government bonds. At the end of 2011, the earnings yield for the aggregate of S&P 500 companies was 4.8 percent, meaning that earnings accounted for 4.8 percent of the market’s value. Versus the 2 percent Treasury yield, the yield gap was 2.7 percent, which was below the 4.7 percent peak at the 2009 market bottom, but well above the historical median of zero percent, as you can see in the display below.

The yield gap can tell us a lot about the future performance of equities versus bonds. Looking at data going back to World War II, my colleague Brian Lomax found a very strong correlation — 90 percent — between movements in the yield gap and the 10-year forward performance of equities versus Treasuries.

Brian also studied the frequency of equity outperformance versus Treasuries in rolling forward one-, three-, five- and 10-year intervals since 1946, generally and when the yield gap was above zero at the beginning of the period studied. In both cases, stocks beat bonds more often as the time periods lengthened, as seen in the display below. The S&P 500 beat 10-year Treasuries in about 87 percent of all 10-year periods. But it outperformed in 99 percent of the 10-year periods that started with the yield gap above zero.

This historical analysis says nothing about near-term timing, and the past is not necessarily prologue. But with the US Federal Reserve promising to keep interest rates at current ultralow levels through at least 2014, we think that today’s unusually wide yield gap makes a persuasive case for an equity-market comeback. As I’ve written before, we get a similar reading from another key gauge, the equity risk premium, which at 8.2% suggests that investor fear of equities is at a 50-year — and, in our view, unsustainable — high.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio-management teams.

Joseph G. Paul is Chief Investment Officer of North American Value Equities at AllianceBernstein.