The purpose of fixed income for most investors is to generate income and serve as ballast in their broader portfolios. It’s not meant to be the fastest boat in the water but, rather, the most seaworthy. Since the 2008–’09 global financial crisis, major central banks have kept interest rates at rock-bottom levels and provided abundant liquidity through asset purchase programs, commonly known as quantitative easing. Time and again, over the past half-dozen years, policymakers and investors alike expected the monetary exertions to resuscitate flagging economic growth, only to push further out on the horizon the anticipated end to ultra-easy money when the growth rebound didn’t materialize. As a result, low fixed-income yields across the developed world have persisted, as has the intense volatility and dispersion in total returns among the many subclasses of bonds within the bond market.

Investors have tried a variety of strategies to hedge interest rate risk and generate some income in this challenging environment. The barbell approach focuses on a combination of short-term bonds to hedge interest rate risk and long-term bonds to produce income with higher yields. But short-term bonds yield little, whereas long-term bonds are more subject to market price risk and so are much more volatile.

The bullet strategy concentrates in bonds of a specific duration or maturity, which in recent times effectively meant very low yielding short-term bonds, given the widespread expectations of U.S. interest rate rises. Investors may take on more credit risk to compensate for the low yields of short-term paper.

A more recent exotic strategy — unconstrained bond funds — seeks to time rising interest rates generally by shorting U.S. Treasuries using interest rate futures. Investors must accurately time the increases for the bets to pay off sufficiently to cover the costs of carry and opportunity costs of not investing in more income-generating instruments.

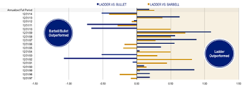

These three approaches have generally faced a major headwind to performance in recent times. After six years, benchmark U.S. interest rates remain at near-zero levels, as the economic recovery following the financial crisis didn’t prove durable. The economy stumbled along at a roughly 2 percent annual GDP growth rate from 2009 through 2014. The economic acceleration last year generated newfound hope that this time around the recovery will prove sustainable enough to prompt the U.S. Federal Reserve finally to begin raising key rates in the second half of 2015. (see chart 1; click to enlarge)

Chart 1: Laddered Structure Outperformed Barbell and Bullet Structures (Difference in total returns as of December 31)

Source: Bloomberg and Thornburg Investment Management. Portfolios are based on Merrill Lynch Bank of America Municipal Indexes. Past performance does not guarantee future results.

Laddering is a time-tested approach to fixed-income investing that allows portfolio managers to focus on fundamental credit research while managing interest rate risk. A laddered portfolio comprises bonds of staggered maturities, with only a portion of its holdings maturing each year. The proceeds from maturing bonds are reinvested in long-dated high-yielding bonds at the top end of the ladder, helping to mitigate the reinvestment risk throughout interest rate cycles.

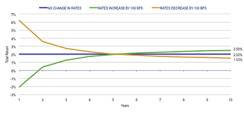

The strategy captures the price appreciation as bonds in the portfolio age to maturity and, in a rising interest rate environment, benefits from the higher rates at which new long-term bonds are issued. If rates don’t rise for a sustained time — as we’ve seen in recent years — the portfolio still generates a steady annual return that is fairly close to the high-yielding bonds in the portfolio. And when the rate cycle peaks and lower rates are on the way, the portfolio’s return gains as bond prices are marked up. As these bonds mature and are reinvested in low-yielding bonds, the portfolio’s long-term return is lower than in rising or stagnant rate periods. But the income stream only gradually decreases as the long-term high-yielding bonds remain in the portfolio. Meanwhile, the portfolio volatility is moderated, thanks to the greater price stability of the limited- and intermediate-term portions of the portfolio. (see chart 2; click to enlarge)

Source: Standard & Poor’s and Thornburg Investment Management. For illustration purposes only, not representative of an actual investment.

Laddered portfolios focus primarily on noncallable bonds. The rungs of the ladder are built from bonds with certain repayment dates, without risk of early redemption. With callable bonds, issuers can repay the bonds early and sell new bonds if the prevailing rate environment becomes more favorable for them. Laddered portfolios usually buy bonds intended to hold to maturity. Hence fundamental bottom-up credit research is critical for laddered strategies, which typically have rigorous criteria for assessing a bond’s price as well as the creditworthiness and willingness of its issuer to service the bond.

Laddering facilitates the focus on active credit research and monitoring of holdings, rather than trying to structure a portfolio around what interest rates might do down the road. As portfolio holdings are all high-conviction, many aren’t sold before they mature, reducing trading costs. To be sure, some may be sold if there’s fundamental deterioration in the issuers’ finances, or perhaps a more attractive opportunity comes along that needs to be financed with a less attractive current holding. But such sales aren’t done for tactical reasons, so they don’t drive turnover in the laddered portfolio, which takes a more strategic approach.

A laddered portfolio has the potential to provide steady returns, thanks to its consistent reinvestment of proceeds from maturing bonds in new, long-dated issues. In addition to mitigating interest rate risk, laddered portfolios can boost portfolio returns by focusing primarily on fundamental credit research and monitoring, helping ensure that only the most attractively priced bonds from solid issuers make it into the portfolio. Holding more bonds to maturity keeps trading costs in check. Among fixed-income vessels, laddered portfolios may not be the flashiest boats on the water, but for decades laddered strategies have provided investors with relatively smooth, buoyant returns, stabilizing their broader portfolios along the way.

Josh Gonze is a fixed-income portfolio manager and managing director at Thornburg Investment Management in Santa Fe, New Mexico.

Get more on fixed income .