It’s never easy to know exactly how an active manager generates returns in complex equity markets. High-conviction strategies can provide greater transparency about the sources of returns — and help create more consistent equity outcomes.

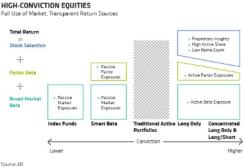

Part of the appeal of passive investing results from market innovations. In traditional active portfolios, the sources of returns were often a gray area (see chart 1). Investors couldn’t always tell how much of a manager’s returns were coming from the market, factor exposures or manager skill.

Today, investors can buy two components of equity returns — broad-market and factor exposure — fairly cheaply, through index funds and smart beta strategies. There could be an opportunity cost for choosing these low-conviction options, however. With returns across asset classes likely to be much lower in the coming years than in the past three decades, we at AllianceBernstein think that forgoing returns from stock selection for the perceived simplicity of passive solutions could leave investors far short of their goals.

High-conviction equity strategies offer another way. They allow investors to access full use of the equity market while also making it much easier for investors to know how much of a strategy’s returns is actually being derived from a manager’s research insights. This framework can help investors ask portfolio managers better questions about their methodology. It can also help investors gain more clarity about how a portfolio will perform in different environments.

Conviction is more than just high active share or concentrated portfolios. Both are important expressions of high-conviction investing, sure; but they do not provide insight as to a manager’s skill. Portfolios that differ from the benchmark or hold small numbers of stocks might have large positions that don’t do well and drag down absolute and relative returns.

We have a much broader definition of skilled, high-conviction investing. First, high-conviction portfolios must have a clear investing philosophy backed by strong research capabilities. These characteristics help ensure that a portfolio manager isn’t just taking outsize positions arbitrarily. Second, a disciplined process is crucial. And third, a high-conviction portfolio must differ meaningfully from the benchmark.

Viewed through this lens, conviction can take many forms. It might be an emerging-markets equities manager with a clear growth philosophy. Even more defensive portfolios focused on dividend-yield stocks or stocks with lower-volatility characteristics can be considered high-conviction strategies if they take a consistent tack. These approaches can all reflect conviction and can be implemented in diversified portfolios with high active share or concentrated portfolios with a small number of stocks.

Our research shows that different types of U.S. high-conviction equity managers have a solid track record, versus the S&P 500 index and passive factor indexes, and have delivered strong risk-adjusted returns over time. We believe that high-conviction equities can be used for a variety of targets, from reducing downside risk to generating income to capturing more upside in rising markets (see chart 2).

Equity investors today face a bewildering array of choices — and big dilemmas. Should you channel increasing portions of an equity allocation toward passive strategies? How can you plan appropriately for an extended period of relatively low returns from all asset classes and still meet your long-term objectives? To make an equity allocation work harder, the portfolios that you pick matter. We believe that rethinking how high-conviction strategies are chosen can help investors ensure that money spent on active management is deployed effectively — and appropriately — for their individual goals.

Sharon Fay is head and CIO of equities, Dianne Lob is senior managing director of equities, and Nelson Yu is co-head of equities quantitative research; all at AllianceBernstein in New York.

See AllianceBernstein’s disclaimer.

Get more on equities.