Can a registered investment adviser (RIA) construct a portfolio structured along the lines of the endowment model? A good place to start to answer this question would be with another question: If you could do it, why would you want to?

The answer to this second question is performance. According to the National Association of College and University Business Officers (NACUBO)–Commonfund Study of Endowments, for the ten-year period ending June 30, 2014, endowments with at least $1 billion in assets (see chart 1) — the group that has most fully implemented the endowment style — had an average annualized return of 8.2 percent. That’s better than the S&P 500 index return of 7.8 percent, the Barclays U.S. Aggregate Bond index return of 4.9 percent and certainly all the blends of those two represented assets that serve as benchmarks for many investors. Plenty of critics felt that the endowment style struggled through the 2008–’09 financial crisis, although taking the long view is a central characteristic of endowment-style investing. And with a ten-year horizon, the endowment model seems to have done just fine.

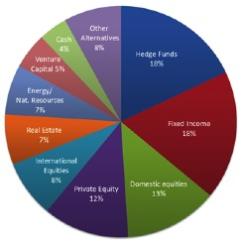

Individual practitioners might differ on specific elements of the definition, but the endowment model typically features the following:

• an equity bias reflecting tolerance of short- and intermediate-term volatility of returns

• a well-diversified asset allocation with a significant portion of alternative investments

• a long-term investment horizon with a mix of liquid and illiquid investments

• an emphasis on total return, ignoring the specific type of income and its tax character.

Obviously, these characteristics represent a long list of asset classes, though it’s important to consider that, because most of the benefits of portfolio diversification are achieved through asset allocation, having within each asset class a relatively concentrated set of investments is both adequate and desirable. This makes portfolio implementation less daunting than it otherwise might seem. Depending on the research resources available, an RIA might rely on a very small number of passive or active equity and fixed-income managers, and either a fund-of-funds or a well-chosen short list of managers to cover the alternative categories. RIAs should feel free to overweight or underweight allocations to the asset categories. If they believe they have a research edge in real estate but not much insight into venture capital, for example, their recommendations should be tilted accordingly.

Building an endowment-style portfolio requires long-term thinking. Only after seven to ten years will the investor know whether the illiquid parts of the portfolio are adding real value. Furthermore, the investor assumes the risk of being unable to make wholesale asset allocation changes frequently or to raise large amounts of liquidity as the portfolio matures.

Assuming an investor is comfortable with those limitations, risk analysis of the alternative investments — and therefore the entire endowment-style portfolio — can be confounding. Even experts differ on how to properly calculate volatility and correlation statistics for illiquid investments. Before recommending a heavy dose of alternative investments, an RIA should have a solid understanding of the diversification provided and should not rely solely on historical statistics. For example, one private equity firm might have generated its past performance primarily by using leverage on a portfolio of companies similar to those in the S&P 500 index. In that case, little fundamental diversification to domestic public equities is provided. Another private equity firm might have unlocked substantial value by promoting changes in strategy and personnel for a handful of companies, and, therefore, the results are likely to offer much greater diversification potential.

Nonetheless, it’s essential to recall that even a well-diversified portfolio does not guarantee steady returns. The 2008–’09 financial crisis hit endowments hard, not to mention traditional portfolios. Given that none of us can predict the nature of the next recession, a diversified portfolio should provide some level of comfort to the investor and the RIA alike.

Finally, whereas endowments benefit from their tax-free status, individual investors need to take additional consideration of tax issues. Given the complexity and lack of short-term flexibility in most alternative-investment portfolios, I would not advise trying to select these investments on the basis of tax treatment. The good news is that many alternative investments are reasonably tax-efficient by their nature, often offering long-term capital gains for significant portions of their total book income. Of course, the traditional stock and bond portfolios can be managed more aggressively for tax purposes. Passive approaches will be somewhat tax efficient, and there are strategies for explicitly taking advantage of the tax code by harvesting losses and postponing gains. The combination of a tax-efficient traditional portfolio and a well-diversified alternatives portfolio should result in an acceptable overall tax profile and the potential for strong risk-adjusted returns over time.

An endowment-style portfolio is no panacea, and is clearly unsuitable for many investors. For investors with a long-term horizon and a tolerance for short-term volatility, though, the endowment style reflects the best ideas of some of the most successful institutional investors.

Don Fehrs is principal, risk management and research, at Evanston Capital Management in Evanston, Illinois. He is also the former CIO of Cornell University’s endowment.

Get more on endowments and registered investment advisers.