A bond with a negative yield seems an absurd investment, as one is guaranteed to lose money unless you can sell it on for an even lower yield. For a foreign investor, however, it is possible — metaphorically speaking — to turn fixed-income lead into gold, as the impact of currency hedging has the curious effect of boosting returns into positive territory.

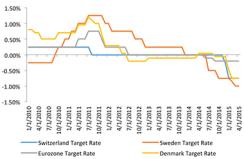

This is not a theoretical exercise. Despite the recent sharp backup in government bond yields, 6.7 percent of the Bank of America Merrill Lynch World Sovereign Bond index, worth some $1.8 trillion, was still trading at negative yields as of June 16 (see chart 1).

Chart 1: Policy rates in negative territory (calculations: Investec and Bloomberg)

By buying foreign sovereign bonds, an investor implicitly takes a long position in the currency in which it is denominated. It is possible for investors to hedge this currency exposure through forward foreign exchange contracts, in which two parties agree to trade a set amount of one currency for another at a predetermined exchange rate in the future, effectively locking in the rate on the day the investment was made.

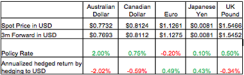

To avoid risk-free returns, a relationship known as covered interest rate parity must hold. If the foreign market has a higher interest rate than does the domestic market, the forward price of the foreign currency will be lower than its spot price, to reflect the higher interest rate earned, thus removing the possible riskless return. The effect of this is for yields on foreign bonds to converge closer to an investor’s domestic market return. For example, a U.S. dollar-based investor, subject to the domestic policy rate, will receive the following annualized hedging return when selling spot and buying three months forward (see chart 2):

Chart 2: Spot and forward rates in U.S. dollars (calculations: Investec and Bloomberg)

By hedging the currency risk, this hedging yield becomes a significant component of total return that must be considered when assessing performance. International investors should take this yield into account when determining expected total return.

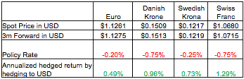

In the topsy-turvy world of negative interest rates, hedging costs are positive (see chart 3). In some cases, this generates a significant pickup in the return profile of this investment.

Chart 3: Spot and forward rates of those countries with a negative policy rate in U.S. dollars (calculations: Investec and Bloomberg)

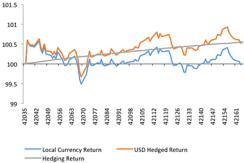

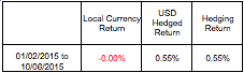

Switzerland demonstrates how this return translates in practice. The yield on the Bank of America Merrill Lynch three- to five-year Swiss government bond index is –0.56 percent. A local buy-and-hold Swiss investor is guaranteed to lose money. From a foreign investor’s perspective, however, returns are very different when combined with an annualized hedging yield on the currency (see chart 4).

Chart 4: Swiss 3–5-year index total return, February 1 to June 10 (calculations: Investec and Bloomberg)

Over the past three and a half months, the local currency return on the index has been zero. The U.S. dollar-hedged return was 0.55 percent, however. On an annualized basis, this is close to 1.5 percent, despite a zero return from the bond itself. Financial alchemy indeed.

Russell Silberston is a fixed-income portfolio manager, and Alex Holroyd-Jones is a multiasset investment analyst, both at Investec Asset Management in London.

Get more on fixed income.