High fees and poor performance are a toxic combination for actively managed funds. According to our research, the largest active U.S. mutual funds investing in European stocks underperformed the STOXX Europe 600 index by 17 percentage points on average over the past 12 months. A failure to generate alpha is among the key drivers behind the emergence of index investing, which, in turn, is raising questions about the relevance of active managers investing in Europe.

A lack of investor conviction in portfolio managers’ ability to beat the market has sparked a shift toward passively managed funds. Exchange-traded funds have enjoyed a wave of popularity since the 2008–’09 financial crisis, and last year saw the highest amount of inflows to Europe to date. Projections show that this record will be broken again this year, with the European ETF industry on track to reach $500 billion in the coming months.

Strategies tracking an index are attractive to investors for two reasons. First, index funds have lower fees, typically around 0.50 percent of invested client money. Second, European markets have rallied significantly in the years since the recession. During the past two years, the Euro STOXX 50 index, which includes the largest European stocks, gained 39 percent. This level of performance has lured more investors into cheaper passive funds.

It is perhaps not surprising, then, to see very significant demand for U.S.-based indexed funds, including ETFs and mutual funds, investing in Europe. Since June 2014, such funds have seen inflows of $24.6 billion, according to Lipper and Nasdaq. At the same time, there has been a growing aversion to actively managed funds. From September 2014 to January 2015, investors withdrew an aggregate $4.4 billion from actively managed funds focused on European stocks.

Yet economic and political shocks could apply the brakes to this trend and reverse it rapidly. A recent survey from PricewaterhouseCoopers indicates that an extreme market event could highlight the risks associated with ETFs and dampen investors’ enthusiasm.

European markets are not immune to such a reality check. For one thing, debt-to-GDP ratios in France, Spain, Italy and Greece stand at 95 percent, 97 percent, 132 percent and 176 percent, respectively. Speculation about a Greek exit, or Grexit, from the euro zone, has risen sharply along with the risk of default, which will come to pass if the country doesn’t get another bailout extension at the end of June. Second, populist, euroskeptic political parties are gaining traction in a number of European countries. A recent poll showed that Marine Le Pen, leader of France’s ultranationalist party, Front National, would win 30 percent of the vote in the next French presidential election. Should euroskeptic parties continue to gain power, it could have adverse effects on European financial markets.

Actively managed equities can prevent significant losses of capital, among other things. By choosing to diverge from underlying indexes, active managers can construct portfolios that may be less sensitive to economic and geopolitical events and are better able to protect investors during volatile times. Equities that exhibit a low or negative correlation to European indexes such as the STOXX Europe 600, which passive funds tend to replicate, fare better during sharp market declines.

The simplest way to measure a portfolio’s potential to safeguard investors is to identify its active share, or the degree to which a fund’s portfolio differs from that of its underlying index. Mutual funds are increasingly disclosing such information.

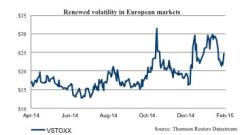

The current environment may present an opportunity for active management to regain some ground in Europe. The correlation among the 50 European biggest stocks fell by 12 percent from November 2014 to January 2015. Moreover, the VSTOXX, which measures the volatility of the Euro STOXX 50 index, has bounced back from yearly lows in June 2014. A decrease in correlation coupled with an increase in volatility provides a chance for active managers to outperform their underlying benchmarks.

It’s prime time for asset managers to underscore their value proposition to clients. Investors are watching.

Nicolas Hourcard is a European equities analyst with Nasdaq Advisory Services in London.

The opinions expressed in this article are those of the author and don’t necessarily reflect those of Nasdaq.

Get more on equities .