In George Lucas’s classic film series, Star Wars, the “Force” is described as an energy field created by all living beings that surrounds and unites galaxies. Today the Force seems to reside with the world’s three most powerful central bankers: the Federal Reserve’s Janet Yellen, the European Central Bank’s Mario Draghi and the Bank of Japan’s Haruhiko Kuroda.

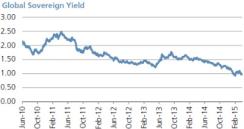

The central banks have been absorbing a significant portion of the net supply of high-quality sovereign bonds, even as the Federal Reserve completed its quantitative easing in 2014 (see chart 1). This demand has pushed aggregate sovereign yields to incredibly low levels (see chart 2), while at the same time global credit spreads remain wider than their long-term average.

Chart 1: Aggregate Central Bank Balance Sheets Continue to Rise as a Percent of GDP

Source: European Central Bank, Statistical Office of the European Communities, Bank of Japan, Cabinet Office of Japan, Federal Reserve Board, Bureau of Economic Analysis, through fourth-quarter 2014. Bloomberg, as of March 30.

Chart 2: Global Sovereign Yields Continue to Fall

Source: Bloomberg, as of March

The Force can bring sovereign yields down. It can punish depositors for holding cash through negative rates. It can also encourage risk-taking as investors search for high-yielding assets to escape financial constraints. This risk-taking can support prices of assets that central banks are not directly buying. This asset price appreciation can even support real economic growth through wealth effects. The jury is still out on the sustainability of that growth. We will leave that to future historians.

The next possible disruption to the Force will be when the Fed begins hiking U.S. rates. Our base case is around the third quarter of 2015. The Fed has attempted to reduce some volatility associated with the rate hike by lowering its dot-plot forecasts for 2015 and 2016. Nonetheless, the implication for investors is, first, to keep some dry powder with the aim of taking advantage of a disturbance in the central bank’s Force and, second, to be armed with the fundamental research for when that disturbance creates opportunities in given sectors.

The central bank policies provide not only a lot of interesting opportunities in the credit markets but also a number of potential pitfalls. We evaluate credit using three broad considerations: fundamentals, technicals and valuations.

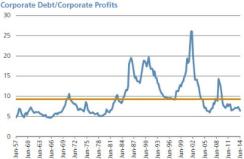

Fundamentals. Broadly, corporate debt levels relative to profits appear to be in line with long-term averages (see chart 3). Additionally, improving economic fundamentals in the U.S. — as evidenced by the declining unemployment rate and incremental cash in consumers’ pockets by way of lower energy costs — provide a supportive backdrop for credit. Similarly, in Europe, stabilizing and improving purchasing managers’ index data support credit fundamentals.

Chart 3: Corporate Debt Looks in Line With Long-Term Averages

Source: Haver Analytics, as of December 2014

Technicals. This is where central bank policy, particularly in Europe and Japan, remains most supportive for global credit. By making deposit rates negative and buying sovereign bonds, the European Central Bank and the Bank of Japan are pushing investors to look for other sources of yield. Globally, high-quality credit should benefit from this as investors look for relatively safe but higher sources of yield.

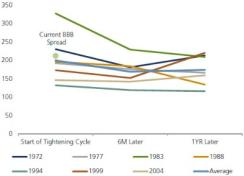

Valuations. Current credit spreads are wider than the long-term average, making for an attractive entry point. Additionally, during prior rate hike periods we have seen credit spreads tighten over time, since rate hikes are also associated with improving economic growth, which helps credit fundamentals (see chart 4).

Chart 4: BBB Credit Spreads Have Tightened in the 12 Months Following the First Rate Hike in Each of the Last Eight Hiking Cycles

Source: Moody’s, Haver; current spread as of February 28

In the U.S. housing-related credits, banks and sectors tied to more consumer-spending power, like auto sales, airlines and lodging, look attractive. In Europe we like peripheral sovereign spreads, exporters that benefit from a weaker currency and subordinated bank securities.

At the same time, it is also important to avoid going to the Dark Side — companies whose valuations are not justified by fundamentals but are artificially supported by central bank policies. To us, these would include select U.S. retail and technology companies that face risks of obsolescence in business models. Similarly, in Europe credit spreads of many corporates now trade tighter than the sovereign spread and hence look less attractive. Finally, in the Asia-Pacific region we expect downside risk to Chinese steel demand to translate into weakness in metals and mining companies in the region. The Force cannot make corporate managers smarter. It does not change the competitiveness of a company. It does not make products suddenly more appealing, and it does not make a secularly declining business profitable.

By virtue of their large balance sheets, central banks today are more powerful than ever. Instead of being choked by negative or negligible yield on sovereign bonds, investors should look for opportunities elsewhere when seeking superior returns. Along similar lines, fundamental credit research is now more important than ever. Focus on companies with improving business fundamentals, high barriers to entry and strong pricing power and those that are delevering. And finally, recognize that this monetary policy reliance globally will likely lead to increased market volatility. Be prepared to take advantage of such opportunities, and may the Force be with you.

Mohit Mittal is a managing director and portfolio manager of investment-grade credit, total return and unconstrained bond portfolios at Pacific Investment Management Co.’s headquarters in Newport Beach, California.

Get more on macro.