After a less than stellar 2013 for bonds, many investors were ready to turn their backs on the asset class. Those who didn’t were rewarded for their long-term perspective. As we at AllianceBernstein see it, investors can derive five lessons from 2014 that provide a rubric for how to pursue fixed-income opportunities this year:

1. Don’t just avoid the crowd — know how to profit from its behavior. Herd mentality is usually a bad idea. Many investors who crowded into higher-yielding debt last year realized too late that they were also increasing portfolio risk. It may have seemed just as straightforward to follow the masses and ditch high yield altogether; however, there were other options. Emerging-markets debt suffered outflows in 2013 but came back into favor in 2014, allowing contrarian investors to profit. As we’ve noted recently, avoiding crowded trades and their unraveling makes sense for many reasons, and so does thoughtful diversification. But don’t miss out on cheap assets the crowd leaves behind.

2. Interest rates aren’t your biggest risk. Many investors sold their short- and intermediate-duration bonds in 2014 because they thought rates would rise. In this low-yield environment — especially for short-term bonds — some investors chased riskier products like higher-yielding triple-C-rated bonds. These low-credit-quality investments should have set off alarm bells, but those investors who didn’t hear them took a beating in the second half of 2014. In our view, now isn’t the time to stretch for yield, and investors should avoid triple-C bonds because they don’t provide enough compensation for the risk they entail.

3. Extreme rallies happen and will happen again. Over a two-day stretch in mid-October, investors across the globe rushed to the perceived safety of ten-year U.S. Treasury bonds. Yield collapsed by 21 basis points, and the price soared by nearly 2 percent. Those may be more severe moves than we’ll see in the very near future, but they are a reminder that liquidity can be challenged even in the most liquid segments like Treasuries. Buying and selling weren’t the problem. The volume of trades was near record levels. The issue was the severe price movement that volume created. Whereas many investors were surprised, the big price jump lessened the concern. Would investors be as complacent if prices fell by 2 percent? Food for thought.

4. Supply and demand continue to drive pricing. For municipal bonds, the past couple of years have been a roller coaster. After mutual fund investors pulled out large sums of money and undermined the market in 2013, municipal bonds enjoyed a revival in 2014. In fact, they’re back with a vengeance. What changed? First, fear-induced selling caused by Detroit and Puerto Rico headlines subsided. And second, investors became more aware of the broadly improving debt picture for most issuers. Sellers became buyers, stoking demand, and supply was nowhere to be found. We expect this dynamic to continue in 2015, which should help support muni bond prices going forward.

5. A stronger dollar left many international bond investors unhinged. Concerns over rising interest rates led many investors to add non-U.S. bonds to their portfolios. A strengthening dollar and negative currency impact left some questioning this approach, however. The Barclays global aggregate bond index (unhedged) returned a paltry 0.6 percent in 2014, compared with an impressive 7.6 percent for the Barclays global aggregate bond index (hedged to U.S. dollars). The difference is currency hedging: eliminating highly volatile currency exposure from risk-reducing bond portfolios can help weather difficult periods such as 2014, when the U.S. dollar was among the strongest currencies in the world. Currency trends tend to last for a few years, so don’t be surprised if this story repeats itself in 2015.

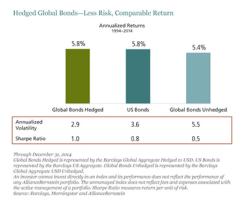

How did currency-hedged global bond returns compare with returns on U.S.-dollar bonds? The Barclays U.S. aggregate bond index returned 6 percent in 2014. Over time, annualized returns for unhedged global, hedged global and U.S. bonds have been roughly the same, but investing in hedged global has been the least volatile choice with the highest risk-adjusted returns (see chart; click to enlarge). The bottom line is that investing in currency is risky. We think core bond investors should consider a hedged global portfolio as their default.

What should investors take away from last year that can be applied to 2015? When it comes to bonds, the best offense is a good defense. Diversification is critical. Investors should continue to pursue a global, multisector approach that’s focused on reducing risk and maximizing opportunities.

Douglas Peebles is chief investment officer and head of fixed income at AllianceBernstein in New York.

See AllianceBernstein’s disclaimer.

Get more on fixed income.