When some future historian sits down to write the definitive economic and financial record of the recent period, we think this chronicler will have a remarkable story to tell. But it will not be the narrative that we have become familiar with in the endless accounts of the 2008 financial crisis. The cast of characters at the Federal Reserve, Treasury and in the private sector will be the same. What will likely have changed is that we will have a better appreciation for the economy’s remarkable technological transformation, which monetary policy response aided, and how it influenced productivity over time.

In the aftermath of the financial crisis, the alphabet soup of innovative rescue programs clearly helped halt economic decline and allowed the private sector to find its footing. Most notably, the Fed’s zero interest rate policy and its successive rounds of quantitative easing helped stabilize the economy and markets — and touched off a remarkable run in risk assets. These policies were timely, bold and appropriately aggressive at that stage. What policymakers had essentially accomplished was buying the economy time to deleverage and, presumably, for fiscal authorities to help, which in and of itself was extremely valuable for letting the system evolve and repair.

Yet in his recently published memoir, The Courage to Act: A Memoir of a Crisis and Its Aftermath, former Fed chair Ben Bernanke lamented that “help was not forthcoming” from Congress in the wake of the crisis. Despite the massive headwinds and the uncertainty it caused, the U.S. economy did eventually deliver. Indeed, we witnessed an extraordinary set of positive influences, including technological development and innovation, a deleveraging of the financial and consumer sectors, a stabilized housing sector and a resurgence in the global competitiveness of a number of industries. Policy also was instrumental in dulling volatility, which was, in turn, key for the market recovery in recent years.

It has taken time, but we believe that the Fed’s employment mandate has effectively been met. From a cyclical peak of 10 percent in October 2009, the unemployment rate stands today at 5.1 percent. Three very solid years of 221,000 jobs (on average) gained each month — with historically low month-to-month volatility — have taken a massive number of qualified applicants out of the unemployment pool. So whereas some cite lackluster August and September nonfarm payroll data this year to downplay the strength of the jobs recovery, we would argue that slowing at this stage is not surprising and, further, that third-quarter payrolls have historically been seasonally weak. Moreover, we have witnessed the most consistent degree of labor market growth in nearly 75 years, all while creating more jobs in the past two years than were created in the prior 13 years. And, most remarkably perhaps, this has occurred alongside a technological revolution that also reduced aggregate job numbers through efficiency gains.

Thus, although many market observers — ourselves at BlackRock included, for a while — believed the Fed was buying time for the fiscal channel to kick in, and grew increasingly frustrated when it didn’t, we now believe that narrative was mistaken. What the Fed’s bought time allowed for was a technological revolution of a kind that will hold tremendous implications for the economy and productivity for many years to come. Examples include: energy sector fracking, the sharing economy, improved data storage and computing power and developments in robotics. It’s quite likely this revolution would have occurred anyway. Economic stabilization in 2009 allowed it to flourish more quickly, however. Some may be surprised that we cite productivity growth, since an argument has arisen in recent years that concludes we reside in a period of low productivity growth, but we believe that, too, is misguided. Technological advances can have a profound impact on economic productivity, the trajectory of future growth and indeed on society as a whole. Yet these influences operate with considerable lags and often in a manner that does not appear straightforward.

Indeed, according to economist Alexander Field’s A Great Leap Forward: 1930s Depression and U.S. Economic Growth, the seeds of greater potential economic output can be sown in times that are not immediately thought of as cultivating prosperity, such as the Great Depression years. Fascinatingly, he argues that it was the confluence of the manufacturing productivity gains peaking in the 1920s and the growth of automotive infrastructure from the 1930s onward that set the stage for successful U.S. efforts in World War II and the following postwar economic boom. We agree that the seeds of innovation that sprout future productivity gains can come at seemingly unlikely times and suggest that the dot-com market crash, the 2008 financial crisis and the subsequent recession may in the future be seen as just such times.

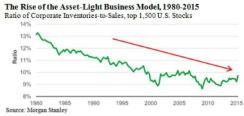

Another example of how technological change is transforming the economic landscape comes in the area of corporate inventory. Whereas some have bemoaned the recent spike in the inventory-to-sales ratio, seeing it as an ominous sign for the recovery, we suggest that a longer-term view of this metric paints a very different picture (see chart 1). It suggests that many corporations, through the use of technology, have refined inventory management practices and have adopted business models that are purposely asset-light. This has had a profound impact on average inventory levels. Indeed, if we look at the top 1,500 U.S. stocks by market capitalization over the past 35 years, we can see that the corporate inventory-to-sales ratio has collapsed by more than 25 percent over that period, from more than 13 percent to less than 10 percent. And as technology further facilitates and encourages asset-light business models in the decades to come, the ratio is likely to drift further downward. We therefore think technological innovation, as well as its disruptive influence on the economy and markets, should not be an ancillary consideration for investors today — but a vitally important one.

Rick Rieder is CIO of fundamental fixed income and co-head of Americas fixed income for BlackRock in New York.