As another new year dawns with hopes that growth will return to precrisis levels, investors have reason to be skeptical. Such expectations have been dashed repeatedly over the past four years. The pattern prompted former U.S. Treasury secretary Lawrence Summers to suggest in a notable recent speech that the American economy may have fallen into “secular stagnation” of subpar output where the natural interest rate, which should balance savings and investment, is negative.

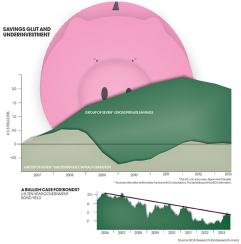

Welcome back to the savings glut! The concept, popularized by Ben Bernanke in 2005 to explain the low level of rates prevailing at that time, is gaining fresh currency and for good reason. The excess of savings over investment in the advanced economies has widened dramatically since the crisis, to some $2 trillion. If that estimate is correct, it would take a prolonged period of stronger output, including higher consumer spending and business investment, to close the gap. Conclusion: The Fed is likely to hold short-term interest rates at zero for some time to come — 2016, anyone? Meantime, there may still be value in bonds — and futures in equity bubble talk.

Get more on investors.