The S&P 500 index passes 1,500. The Dow Jones closes above 14,000 for the first time since the financial crisis. Individual investors start returning money to the stock market.

As encouraging as these stories are, headlines alone don’t make the case that U.S. equity markets will continue plowing ahead. But we think there’s plenty of evidence that 2013 could be the fifth consecutive year that equity investors climb the “wall of worry.”

There are still big-picture risks to get hung up on — that’s been true for years. Lately the potential drag of U.S. fiscal austerity seems to have displaced Europe’s sovereign crisis and the China slowdown as investors’ biggest worry. But despite the preoccupations, stocks finished on positive ground in 2009, even coming off a brutal, multiyear tailspin. They were up again in 2010. And in 2011. And in 2012. Four straight years of positive returns. Volatile, yes, but also up.

Stocks must be getting tired of climbing by now, we hear people say. It’s time for the market to take a rest — or a fall. But when we cut through the emotion to look at the fundamentals, we see promising signs that equity markets have a lot left in the tank.

Home prices have been rising, and new-home activity has been improving. Rising home prices can be a big boon to consumer confidence by shoring up their net worth. It’s a shot in the arm for banks too. And improving new-home construction should help support more job growth.

The run-up in the euro in the second half of 2012 has helped too, bolstering U.S. corporate earnings. That’s because multinational companies with substantial overseas operations are able to translate non-U.S. earnings back into U.S. dollars at a more favorable rate.

Corporate earnings have been at record levels — and are still growing. Earnings per share for the S&P 500 index should check in at about $103 for 2012 — a new high. Dividends, in terms of total dollars paid out, are also at an all-time high and look to be growing faster than earnings. The dividend yield on stocks still stacks up well against bonds. And there’s the upside potential.

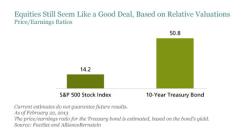

Based on our assessment, equity valuations still look like a good deal — even after an impressive four-year rally. As of late February, as seen in the display below, the S&P 500 was trading at a price-earnings (P/E) ratio of about 14 times. Compare that with the yield of about 2 percent on the 10-year Treasury bond, which works out to an “earnings” multiple of roughly 50 times.

We think investors will increasingly see this as evidence of a good opportunity to return to equities. There have been signs of money in motion: In January 2013 investors put more than $20 billion into U.S. stock funds. That hardly offsets the huge outflows in previous years, but it’s a promising sign. In our opinion, more institutions could also up their equity allocations after cutting them to well under 50 percent over the past decade.

All told, these factors seem to make the case for investors maintaining a strong foothold on their way up the wall of worry in 2013.

It may not be a straight path, as we’ve seen with some of the recent market swings, but we’re pretty confident they’ll keep climbing.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio-management teams.

Kurt Feuerman is chief investment officer — Select Equities at AllianceBernstein.