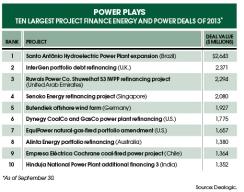

February 2011 was bitterly cold in Texas. Increased power demand for heating overburdened the grid, forcing rolling blackouts. Some 7,000 megawatts had to be switched off, leaving hundreds of thousands of people in cities like Dallas and Houston without electricity for 45-minute spells.

Spot power prices — what utilities pay when their own supply is cut — surged 60-fold, from a typical $50 per megawatt hour to about $3,000 on February 2, 2011. Having shut down several overworked or damaged facilities, grid operators even imported power from Mexico. The chance to sell energy to the Texas grid helped spark the rebirth of U.S. merchant power plants after a few years of dormancy following the global financial crisis; the first new facility was financed in July 2012. If states are energy hungry, institutional investors now appear equally ravenous for merchant plays’ generous yields.

Developers build merchant power plants without contracts with utilities. At the vanguard of the revival is Dallas-based Panda Power Funds, which is constructing three gas-fired plants in Texas and has four more planned for Maryland, Pennsylvania and Virginia. “This market is completely different from anything we have ever seen before,” says Panda senior partner and president Todd Carter, noting that rising electricity demand and cheap shale natural gas have been game changers. “Those projects are just the tip of the iceberg as to the investment needed.”

Panda was launched in 2010 by the former senior management team of Dallas-based independent power developer Panda Energy International. The firm aimed to be the first mover in markets with little surplus power when usage spikes, during heat waves or cold snaps, for example. With natural-gas prices expected to stay low and up to 60 gigawatts of U.S. coal-fired power generation slated for retirement to meet environmental standards, other players, such as Chicago-based Invenergy and Silver Spring, Maryland–based Competitive Power Ventures Holdings, are joining the merchant fray.

Since financing the 758-megawatt, natural-gas-fired Temple I plant in Temple, Texas, in July of last year, Panda has raised about $3 billion in equity and debt from institutional investors. The firm’s strategy is simple. First, it uses equity from the funds it raises. Panda backed the three Texas projects with money from its maiden $420 million Panda Power Generation Infrastructure Fund, whose investors included the State Teachers Retirement System of Ohio, the Indiana Public Employees’ Retirement Fund, the 3M Employee Retirement Income Plan, Dutch pension fund APG, the Alfred I. duPont Testamentary Trust and a large U.K. public pension fund.

Panda then taps the B-loan market to raise debt-backing facilities, with many of its equity investors chipping in. The Ohio teachers’ system provided $50 million in debt for the 829-megawatt Moxie Energy “Liberty” plant in Pennsylvania, which Panda financed in August . “Panda has benefited from its access to equity capital and an aggressive management team,” says Carl Peterson, head of debt origination at GE Energy Financial Services in Stamford, Connecticut. “The B-loan market for financing is also significantly more expansive now,” Peterson adds, citing institutions’ willingness to educate themselves about merchant power and make credit committees comfortable with the risk of not having a guaranteed buyer.

The internal rate of return on an investment in Panda’s fund could be 25 to 30 percent, says Robert Johnston, Boston-based CEO of Beacon Hill Financial, the placement agent for the firm’s first vehicle and for a second one now in the works. As institutional investors hunt for yield in a low-interest-rate environment, they’re open to taking on more risk and are moving from commercial real estate to the energy sector, Johnston notes.

But institutions now also have more buckets into which an investment like Panda might fall, whether they regard it as a high-return, infrastructure or opportunistic play, he adds: “Institutional investors are taking a more sectored approach to the private equity markets.”

Panda has had its share of teething problems. When it closed the debt financing for Temple I last year, pricing on the institutional tranche was high, at Libor plus 1,000 basis points, as investors warmed to the new asset class. Only eight institutions offered debt for that deal. But when Panda financed Temple II this April, more than 70 wanted to supply debt, and the firm secured pricing of Libor plus 650 basis points.

By the end of the year, Panda plans to close a second fund worth between $800 million and $1 billion. All of the investors from the first fund have lined up for a piece of it, and the firm already has about $600 million in commitments. The merchant power renaissance looks to be gathering steam. • •

Read more about capital markets.