Amid the rush to the exits by investors fearful of a so-called bond bubble, one group has been buying, sometimes aggressively. Who are these contrarians? What do they see that the broader public doesn't?

Answer: They are managers of America's corporate pension funds and insurance companies. They are buying long bonds. And their motivations offer lessons to the stampede of sellers.

Understanding their actions requires revisiting the last decade and a half of funding in the pension universe. From a top of 128 percent in 1999, the aggregate funding ratio of pension plans of companies in the Standard & Poor's 500 index fell to 81.6 percent in 2002, slowly climbing to crest again at just over 100 percent in 2007, only to plummet in 2008. Since 2009 the ratio has bounced around 80 percent despite a more than doubling of U.S. equity prices. Last year, the aggregate funding ratio fell to 78 percent, marking the nadir of the last two decades. Would you blame any plan sponsor for reaching for the Dramamine?

As keen observers know, funding is not just about the value of assets, but also liabilities. Pensions have very long-dated liabilities. And the decline in interest rates that fueled the great bond bull market sent liabilities skyrocketing for plan sponsors, and similarly for their cousins on the life insurance side, because these investors use market rates to discount their future liabilities.

Driven by a combination of George Bush's famously botched aphorism, "Fool me once, shame on ... shame on you. Fool me ... You can't get fooled again!" plus accounting and regulatory changes in 2006 that brought heightened focus to funding, pension plan sponsors began to drastically change the ways they managed plan assets.

Since 2009, the dominant thematic strategic change among consultants and plan sponsors has been to adopt derisking glide paths. The idea: As plan funding (gradually) improves, sell risk assets and buy hedging assets — predominantly long investment grade corporate bonds. Funding could improve for one of three reasons:

- Risk assets (e.g., equities) go up.

- Discount rates rise and liabilities go down.

- Sponsors put more money into plans.

Given the rise in risk assets since the beginning of the year, followed by the recent bond sell off — which has seen the 10-year Treasury yield back up nearly 100 basis points since its recent low of 1.63 percent on May 1 — plan funding has had a decided uptick. Milliman estimates aggregate funding is up by 6 points year-to-date through May, and we'd estimate a further 2 to 3 percentage point increase in June. Plan sponsors are cruising through derisking triggers and moving money from equities into long corporate bonds. A few large plans with better funding positions at year-end are either back to full funding or just on the doorstep. Buying of long credit has been strong throughout the year and has increased noticeably in the past few weeks. We anticipate it will continue through the balance of the summer and into the fall. These plan sponsors are happy to get off the roller coaster.

Life insurers find themselves in the same boat. They too have books of liabilities that are very long-dated and face a persistent asset-liability mismatch. Liquid bonds may extend to 30 years, but projected annuity cash flows can extend 40, 50 or more years into the future. These liabilities only get longer as we live longer.

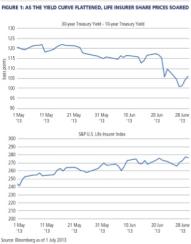

The graphs in Figure 1 show two interesting phenomena since the beginning of May. First, note that as the benchmark 10-year yield rose dramatically, the yield curve between 10 years and 30 years flattened materially, consistent with some support from long bond buyers. Also note that in a period where both equities and fixed income sold off broadly, life insurer stock prices rose more than 10 percent.

Clearly, rising rates have been good for pensions and life insurers.

What about the broader public? Pensions and life insurers have explicit long-dated liabilities. In truth, though, just about everyone saving for retirement has implicit long-dated liabilities. Higher rates ultimately may be good for investors worried about how much they need to save for retirement.

The transition period may be painful, but this current cloud does have a silver lining.

James Moore, a managing director in Pacific Investment Management Co.'s Newport Beach, California office, leads the global liability-driven investments product management team, co-heads the investment solutions group and is Pimco's pension strategist. This article contains the current opinions of the author but not necessarily those of Pimco.